SchusterWatch Q1 2026 Review (4/1/2026)

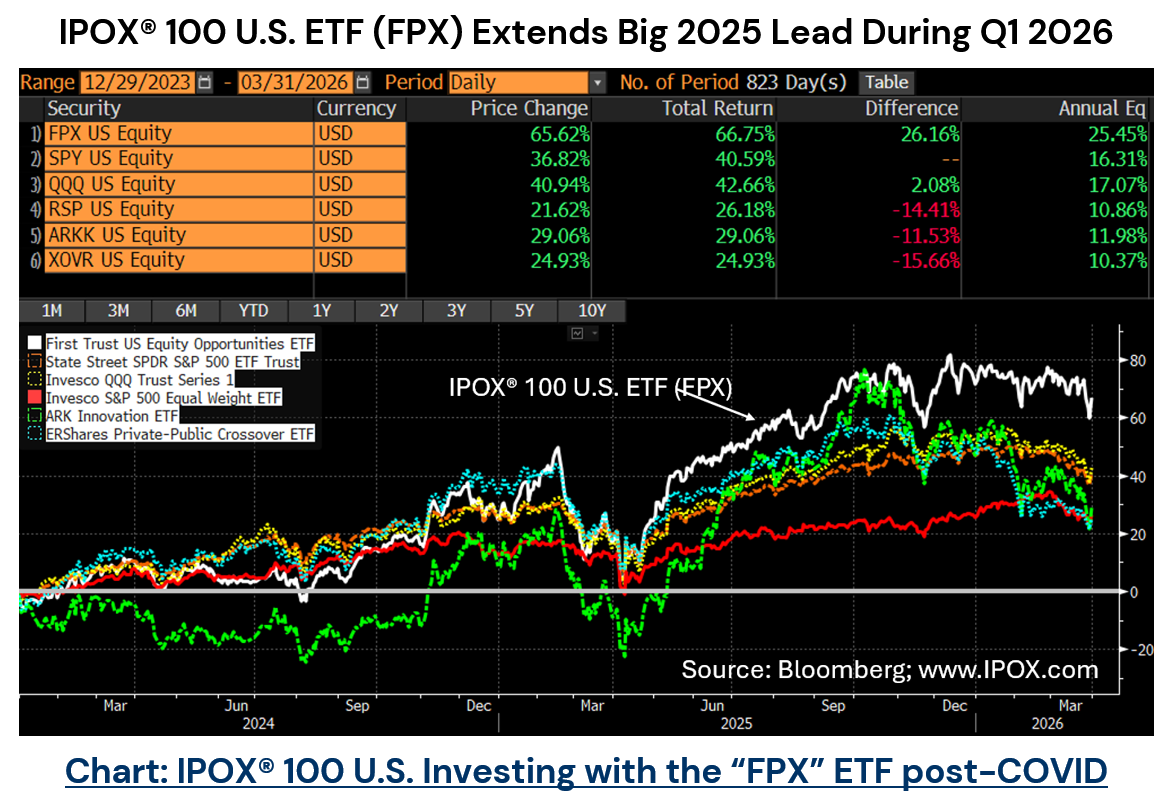

Key IPOX® Indexes extend 2025 Strength during Q1; ETFs: FPX, FPXI, FPXE.

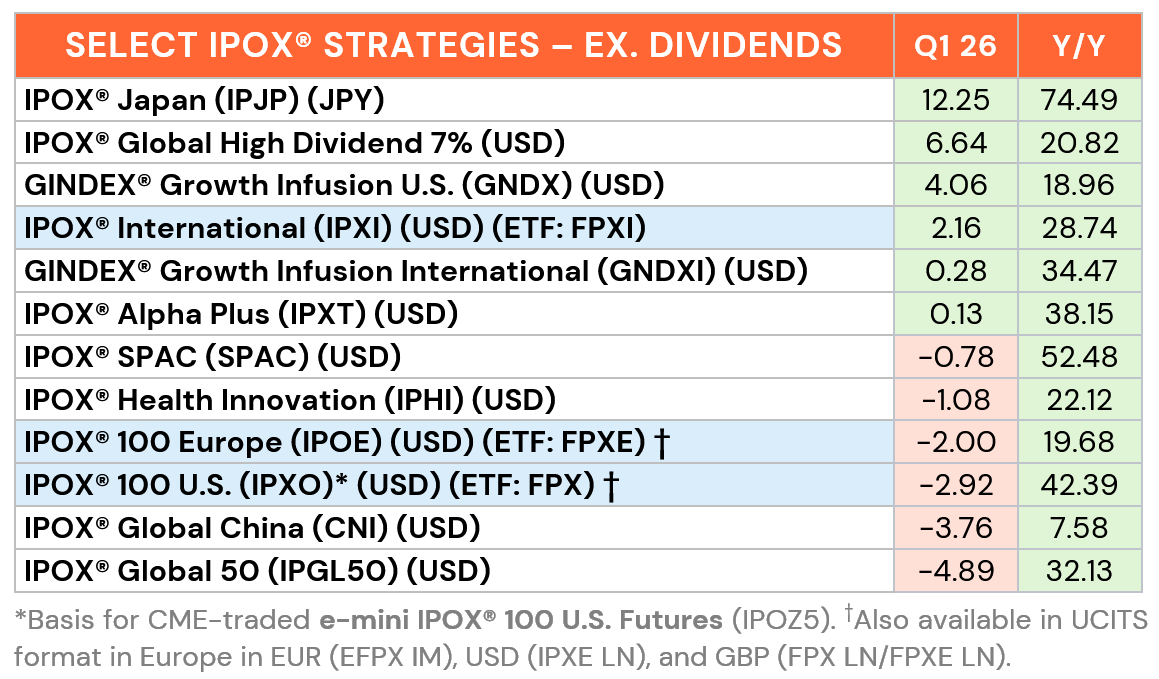

IPOX® Japan, IPOX® Global High Dividend 7% lead Q1 performance rankings.

Movers: Storage, Energy and Biotech help to buffer big losses in Software.

Global Deal Flow: 244 firms go public as IPO proceeds jump to $40 billion.

OVERVIEW: The key IPOX® Indexes traded resilient during Q1 2026 as earnings strength helped to offset much of the negative impact on our investment universe from 1) the AI-driven contraction in multiples in the SaaS sector and resulting credit vows and 2) the heightened economic uncertainty driven by escalating geopolitics resulting in a jump in equity risk (VIX: +68.90%), while interest rates rose at the same time.

UNITED STATES: The IPOX® 100 U.S., key semi-passive U.S. post-IPO performance benchmark and underlying for the $1.5bn “FPX” ETF – declined -2.92% during Q1 2026, +171 bps. and +306 bps. better than when compared to passive U.S. stock benchmarks S&P 500 (SPX) and Nasdaq 100 (NDX), while also outperforming a long list of active ETFs with a high New Listings Factor load, including the ARK Innovation Fund (ARKK: -12.13%). Big losses in SaaS, Crypto and select Financials such as in Sailpoint (SAIL US: -34.55%), SoFi (SOFI US: -39.34%), LegalZoom (LZ US: -42.90%) and Unity Software (U US: -50.33%) were almost offset by big gains in computer storage device makers Sandisk (SNDK US: +167.55%), Lumentum (LITE US: +90.66%), biotech CG Oncology (CGON US: +63.01%) and energy firms Kodiak Gas Services (KGS US: +57.47%) and Knife River (KNF US: +16.06%).

IPOX® High Divi 7%, IPOX® M&A Gain: We note another strong quarter for the active IPOX® Global High Dividend 7%, with the portfolio adding +6.64% during Q1, almost doubling its benchmark. Strength also extended to the Corporate Action-focused IPOX® Growth Infusion U.S. (GNDX), which added +4.06% in Q1, while the IPOX® Alpha Plus (IPXT) rose +0.13%.

INTERNATIONAL: The key IPOX® Indexes focused on non-US stocks held steady during Q1. While the IPOX® Global China (CNI) fell -3.76%, less than the benchmarks, the IPOX® Japan (IPJP) soared +12.25% and the IPOX® 100 Europe (ETF: FPX) shed -2.00%. Exposure to M&A targets, including U.K. biotech Centessa (CNTA US: +58.82%) added significant Alpha to IPOX® Returns. A slew of recent European IPOs, however, disappointed, including British online bank Shawbrook (SHAW LN: -34.16%), Fintech Klarna (KLAR US: -54.72%) and Czech defense play CSG (CSG NA: -6.64%).

THE IPOX® SPAC INDEX: The Index fell just -0.78% during Q1, reflecting resilience despite continued stock market volatility. Activity rose with 16 SPACs announcing merger targets, led by California-based GM EV battery materials supplier Controlled Thermal Resources, agreeing to merge with Plum Acquisition Corp IV (PLMK US) in a $4.7 billion transaction. At least eight SPACs completed business combinations during Q1, including quantum player Infleqtion (INFQ US) which finalized its merger with Churchill Capital Corp X in February. Corporate activity in the deSPAC universe remained active, with multiple firms receiving take-private interest. Among them, 07/2021 deSPAC Reservoir Media (RSVR US) attracted competing acquisition proposals, highlighting ongoing strategic value in select deSPAC assets. On the issuance side, 62 SPAC IPOs in the U.S. raised over $13 billion during Q1, marking a notable the busiest quarter since COVID.

ECM DEALS & OUTLOOK: Global deal count saw 244 listings in Q1 (down from 292 in Q1 2025), with total proceeds jumping to $40.31 billion compared to $27.96 billion last year. Q1 listings delivered strong average aftermarket gains of +35.00% through the quarter's close. In the U.S., 31 deals went public, raising $9.83 billion. Activity was led by data center power provider Forgent Power Solutions (FPS US: +8.41%, $1.74 billion) and Japanese payment processor PayPay (PAYP US: +33.38%, $1.01 billion). However, performance for other sizable U.S. deals was mixed: Construction machinery rental firm EquipmentShare.com (EQPT US: -16.68%, $859 million), space defense firm York Space Systems (YSS US: -34.79%, $629 million), and diabetes med-tech MiniMed (MMED US: -25.40%, $560 million) struggled, though solar provider Solv Energy (MWH US) managed a solid +14.04% gain on its $589 million raise. Internationally, Hong Kong dominated the volume of large deals. Notable listings included pig farm operator Muyuan Foods (2714 HK: -0.31%, $1.55 billion) and energy drink maker Eastroc Beverage (9980 HK: -13.23%, $1.42 billion). Stand-outs included semiconductor firms Montage Technology (6809 HK: +44.07%, $1.04 billion) and Biren Technology (6082 HK: +47.04%, $825 million). The quarter’s largest IPO belonged to the $4.46 billion listing of Czech defense firm CSG (CSG NA), which slipped -6.64%.

Looking ahead to Q2, deal flow is expected to be somewhat subdued amid ongoing geopolitical uncertainty in the Middle East, though the IPO window remains wide open for defense and energy firms. Markets are also closely monitoring the potential return of the “Super IPO”, with SpaceX reportedly preparing to file for a record-breaking $75 billion listing within weeks.