SchusterWatch #851 (07/13/2026)

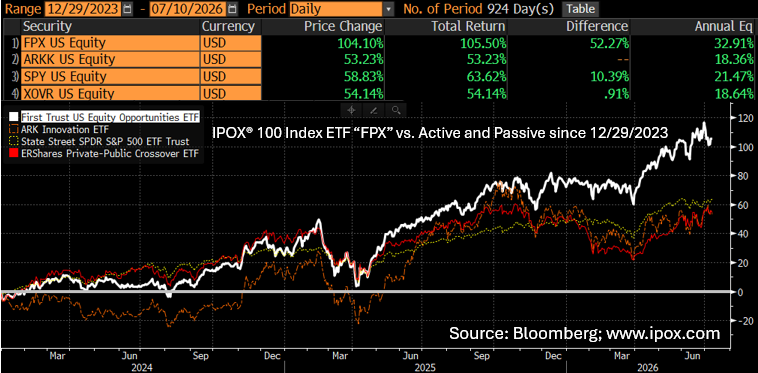

Ahead of Earnings: Following end-of-Q2 gyrations, IPOX® 100 U.S. Index (IPXO) rises.

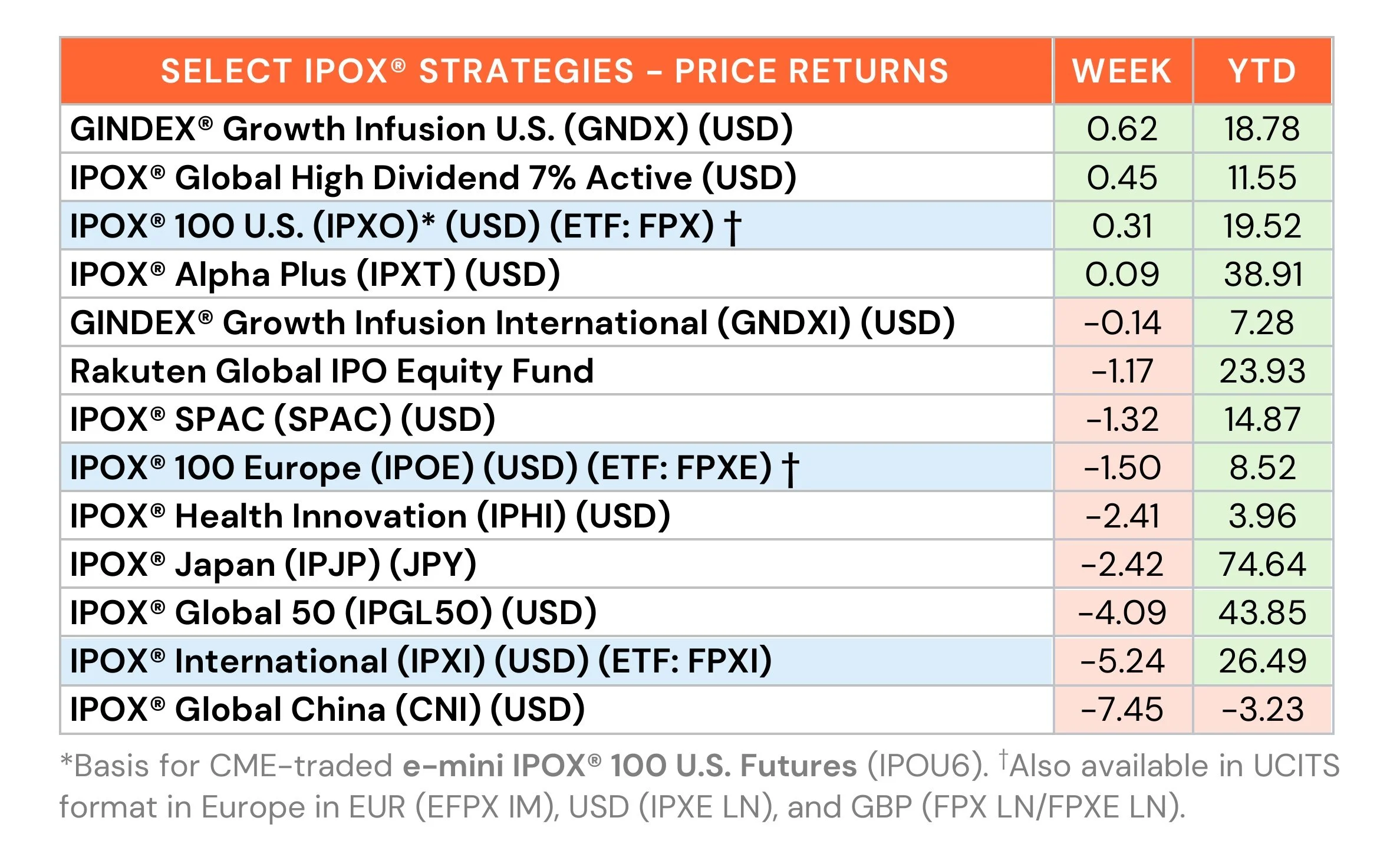

IPOX® Japan (IPJP) maintains massive YTD lead; GINDEX® U.S. reaches weekly ATH.

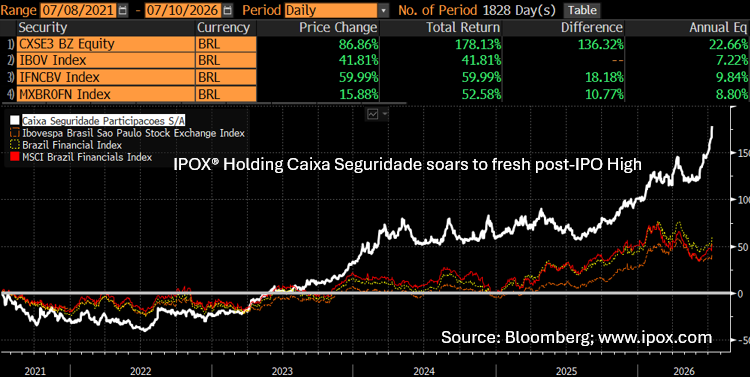

Stock in focus: Brazilian financial Caixa Seguridade Participacoes (CXSE3 BZ)

IPOs: No pops amid massive Deal Flow in H.K.; our coverage of Jersey Mike’s.

WEEKLY OVERVIEW: While the rotation back into AI-related exposure lifted the IPOX® 100 U.S. Index (IPXO) last week, volatility in China, amid massive IPO deal flow in Hong Kong, weighed on international exposure. Against a backdrop of higher U.S. yields and a more range-bound JPY, the broad-based IPOX® Japan (IPJP) strategy maintained its historic lead, while our M&A-focused GINDEX® Growth Infusion U.S. (GNDX) set a fresh weekly all-time high.

U.S: The IPOX® 100 U.S. Index (IPXO), the key innovation gauge tracked by the First Trust U.S. Equity Opportunities ETF (ticker: FPX), added +0.31%, bringing its YTD return to +19.52%, or +886 bps ahead of the S&P 500 (SPX) YTD. 54% of portfolio holdings rose, while the average and median constituents returned -0.26% and -0.09%, respectively, underperforming the IPOX® 100 U.S. Index. The rebound in semiconductor-related stocks, including Ingram Micro (INGM US: +13.29%) and Sandisk (SNDK US: +9.79%), more than offset losses stemming from weakness in SpaceX (SPXC US: -10.31%) and specialty-chemicals maker Solstice (SOLS US: -23.56%), which fell sharply following a deal to acquire Element Solutions (ESI US: -8.75%).

INTERNATIONAL: Following the quarter-end run-up, the IPOX® International Index (IPXI) weakened for a second week. Amid a flood of tech IPOs in the Hong Kong market, which overall delivered limited gains to initial IPO investors, incumbent stocks traded with significant volatility. These included leading battery maker CATL (3750 HK: -13.10%) and semiconductor maker GigaDevice (3986 HK: -13.10%). Key global alternative-energy company Siemens Energy (ENR GY: -9.52%) fell following a significant downgrade, adding further pressure. We note, however, another strong week for Brazilian financial firm Caixa Seguridade Participações (CXSE3 BZ: +7.40%), a key holding in the IPOX® International portfolio. Amid a spike in trading volume and speculation about potential corporate action, the 6.53%-yielding insurance provider closed at a fresh post-IPO high.

SPACS: The IPOX® SPAC Index fell -1.32%, bringing its YTD return to +14.87%. Crypto miner and data-center operator Cipher (CIFR US: +10.33%) rebounded from the previous week’s sell-off. Space-infrastructure firm Rocket Lab (RKLB US: -19.33%) fell sharply amid weakness in SpaceX. One SPAC announced a merger target, with RF Acquisition Corp. III (RFAM US) agreeing to combine with Taiwan-based long-term-care network provider HCC Healthcare. Spring Valley Acquisition Corp. III completed its business combination with Vancouver-based fusion-energy developer General Fusion (GFUZ US), with the combined company expected to begin trading on July 13. Five new SPAC IPOs launched in the U.S. last week.

ECM REVIEW & OUTLOOK: 52 firms completed IPOs globally last week, raising a combined $36.1 billion. The companies rose by an average of +34.61% from the offer price through Friday’s close, with a median gain of +6.19%. The headline transaction was the secondary U.S. listing of Korean chipmaker SK Hynix (SKHYV US: +12.76%), which raised $26.51 billion.

Europe saw the IPO of Swiss hospital-property company Infracore (INFRAC SW: -0.46%, $281 million offer). The week’s most notable Hong Kong deal was the listing of electronics manufacturer Luxshare (2475 HK: -0.44%, $3.09 billion), followed by chip-components maker Three-Circle Group (6951 HK: +4.69%, $913 million), Nexchip Semiconductor (2249 HK: 0.00%, $890 million), and self-driving-technology company Momenta Global (6880 HK: 0.00%, $751 million). Other deals included CNC-milling specialist Dtech Technology (1377 HK: +1.58%, $612 million), autonomous-mining-vehicle developer Eacon Group (7687 HK: +2.48%, $293 million), chemicals company Befar Group (6745 HK: -18.68%, $156 million), and oscilloscope specialist Rigol Technologies (537 HK: -40.63%, $145 million).

This week’s calendar includes the U.S. IPOs of data-center infrastructure provider Csquare (CSQR US, $1.25 billion), nuclear-fuel company Standard Nuclear (STDN US, $356 million), and eye-disease biotechnology company Tarsier Pharma (TARX US, $45 million). Europe’s deal flow is led by SMAG, a German defense manufacturer of mobile communications masts (1SMA GR, $175 million), and Italian gold and jewelry retailer Gens Aurea (OROX IM, $127 million). Following Jersey Mike’s S-1 filing, the latest IPOX® Watch Pre-IPO Analysis takes a closer look at the sandwich chain, confidential filer and restaurant holding company Inspire Brands, and the broader restaurant IPO landscape (Read here).