SchusterWatch #850 (07/06/2026)

Yield Relief: Weak jobs, lower oil prices support equities, as profit taking hits AI sector.

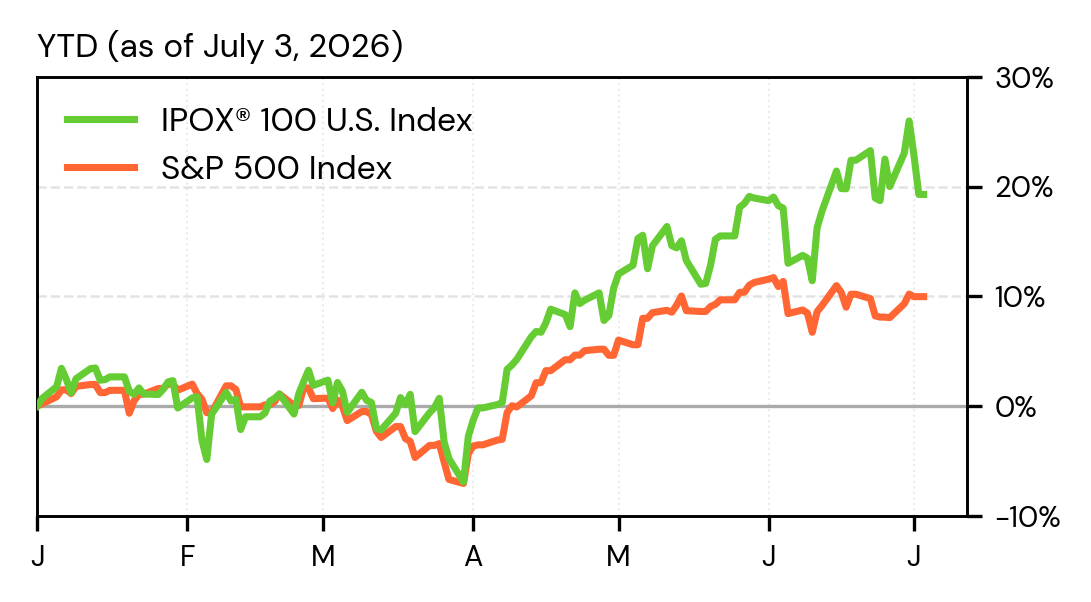

Holding the lead: IPOX® 100 U.S. at 19% YTD, maintaining +1173 bps vs. S&P 500.

Movers: Viasat, Rivian, AST SpaceMobile, Reddit, Kelun-Biotech, Siemens Energy.

IPOs: Hong Kong drives $7.3B calendar, Jersey Mike’s and Cumberland Farms file.

WEEKLY OVERVIEW: During the shortened Fourth of July trading week, lower yields supported equities after weaker U.S. jobs eased Fed rate-hike concerns and falling oil prices reduced near-term inflation pressure. The IPOX® Indexes traded mixed, with Space and Healthcare exposure providing support, while a large rotation across select AI and semiconductor exposure, profit-taking in recent winners and concerns over debt-funded AI spending weighed on the return distribution.

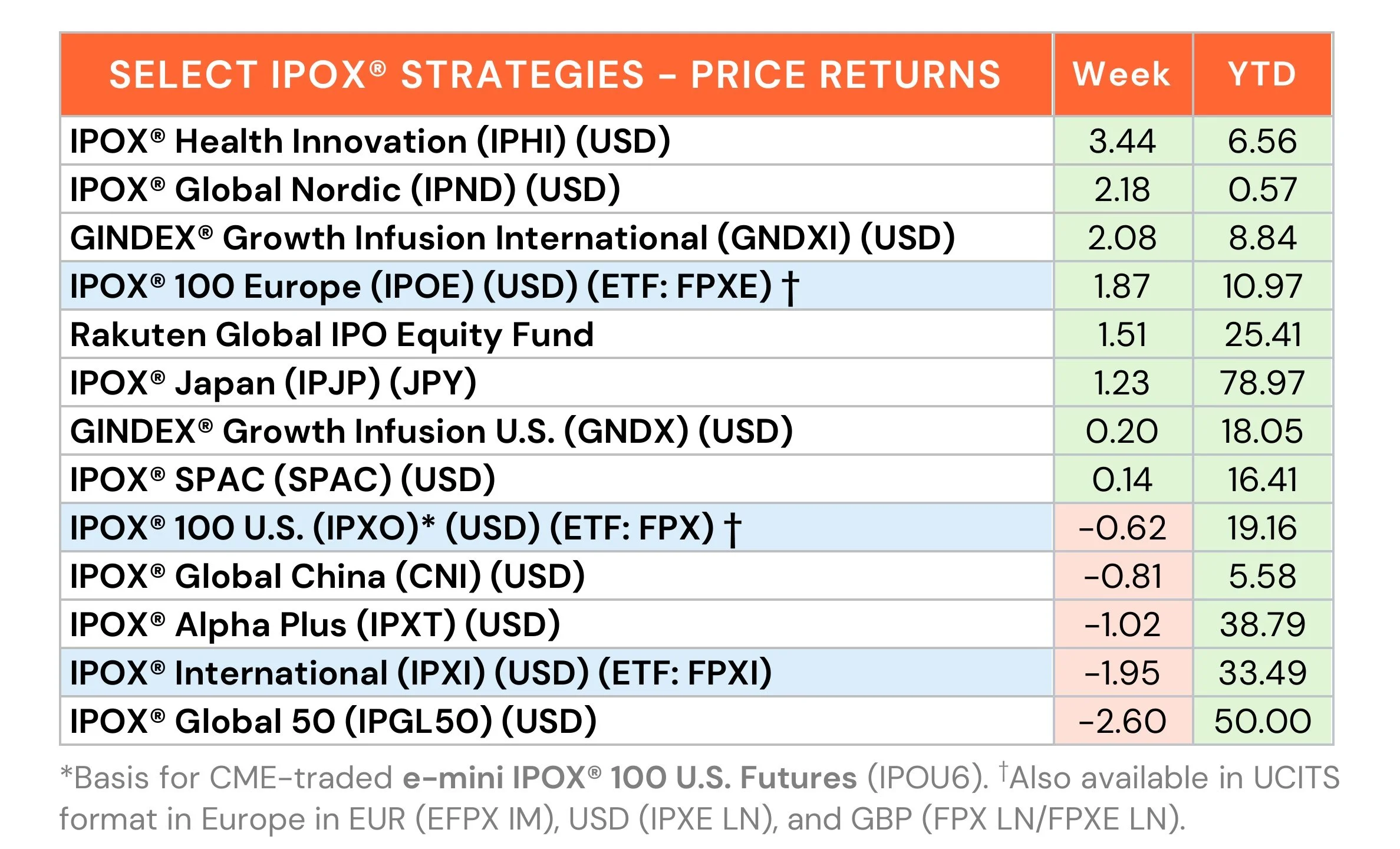

U.S: The IPOX® 100 U.S. Index (IPXO), the key innovation gauge tracked by the First Trust U.S. Equity Opportunities ETF (Ticker: FPX), edged lower by -0.62% to +19.16% YTD, remaining +1173 bps ahead of the S&P 500 (SPX: +7.43% YTD) and +384 bps ahead of the Nasdaq 100 (NDX: +15.32% YTD). The equally weighted IPOX® 100 U.S. gained +0.29% last week, highlighting profit-taking among some of the largest holdings.

Year-to-Date Total Return:

Space was a key factor, buoyed by M&A action around IPOX® Alpha Plus (IPXT) holding Rocket Lab acquiring Iridium. Satellite maker Viasat (VSAT US: +34.08%) gained on U.S. Space Force contracts, while AST SpaceMobile (ASTS US: +19.15%) rose on a JV with Japan’s Rakuten. SpaceX (SPCX US: +5.72%) gained upon addition to the MSCI World ahead of its July 7 inclusion in the Nasdaq 100. Other winners included EV maker Rivian (RIVN US: +19.19%) on higher guidance and social network Reddit (RDDT US: +16.61%) on AI licensing deal renewals. After a big run-up, profit-taking pressured AI plays such as Sandisk (SNDK US: -16.54%), CoreWeave (CRWV US: -15.36%) and Forgent Power (FPS US: -15.00%). Healthcare was another area of strength, with Medline (MDLN US: +11.11%), BridgeBio Pharma (BBIO US: +9.89% on a $1B financing deal), and diabetes management spin-off Minimed (MMED US: +9.48%) standing out, helping the IPOX® Health Innovation Index (IPHI: +3.44%) to lead the IPOX® Indexes for a second week.

INTERNATIONAL: The IPOX® 100 Europe Index (IPOE; ETF: FPXE) added +1.87% to +10.97% YTD, as Eurozone inflation dropped, reducing ECB tightening concerns. Defense exposure rebounded sharply, including shipbuilder TKMS (TKMS GY: +13.51%), equipment firm MilDef (MILDEF SS: +11.66%) and tank component maker RENK (R3NK GY: +10.87%). Sweden’s Ambea (AMBEA SS: +12.91%) surged on news of acquiring rival Humana to create a leading Nordic care provider, also helping the IPOX® Global Nordic (IPND: +2.18%) higher.

As in the U.S., the IPOX® International Index (ETF: FPXI) saw profit taking in select AI-linked names, with Knowledge Atlas (2513 HK: -12.37%), GigaDevice (3986 HK: -15.28%) and Kioxia (285A JT: -9.63%) falling. Offsetting gains included AI electrification play and large holding Siemens Energy (ENR GY: +9.23%), healthcare firm Sichuan Kelun-Biotech (6990 HK: +19.38%) and Canadian gold and copper miner DPM Metals (DPM CT: +10.43%).

THE IPOX® SPAC INDEX: The Index gained +0.14%, bringing YTD gains to +16.41%. Asset manager Abacus Global (ABX US: +19.68%) was the best performer as shares extended momentum. Crypto miner/data center operator Cipher Mining (CIFR US: -22.74%) performed worst. One SPAC announced a merger target, with JATT Acquisition Corp II (JATT US) to combine with Talawar Therapeutics. 2 SPACs completed combinations, including Cantor Equity Partners II with tokenization platform Securitize (SECZ US). 4 new U.S. SPACs launched.

ECM REVIEW & OUTLOOK: 34 firms went public globally last week, raising $7.8 billion. New listings gained an average of +54.17% from offer price to Friday’s close (median: +5.43%). U.S. listings led accessible market activity, with Italian tech acquirer Bending Spoons (BSP US: +23.90%) raising $1.68 billion, followed by telecoms utility firm ITG (ITG US: -3.37%, $359 million). IPOX® Associate Lukas Muehlbauer commented on the debut, highlighting demand for companies tied to AI infrastructure. Uber-backed micromobility firm Neutron Holdings/Lime (LIME US: 0.00%, $174 million) also debuted, with Muehlbauer noting that the reception appeared measured and that Lime must prove it can sustain growth.

Outside the U.S., Hong Kong was led by Chinese home electronics firm Anker (668 HK: +0.53%, $591 million), fibre optics specialist Crealights (1191 HK: +45.88%, $195 million), and kidney pharma Alebund (9637 HK: +33.98%, $164 million). Polish residential developer Robyg (ROB PW: -0.18%, $322 million) also ranked among the largest international listings.

Activity this week is focused mainly on Hong Kong, with expected deal flow of $7.3 billion amid offerings tied to semiconductor supply chains. Manufacturing contractor and Apple AirPods maker Luxshare (2475 HK, $3.1 billion) leads, followed by electronic components maker Three-Circle Group (6951 HK, $913 million), wafer foundry services provider Nexchip (2249 HK, $890 million), autonomous driving firm Momenta (6880 HK, $751 million), and PCB tools maker Dtech Technology (1377 HK, $612 million).

In the U.S., sandwich chain Jersey Mike’s (JMKE US) filed publicly for a NYSE listing, with IPOX® Associate Lukas Muehlbauer commenting in Reuters. Convenience-store operator Cumberland Farms also advanced IPO plans, with IPOX® VP Kat Liu in the News. Copper products maker Londian Wason New Energy Tech also filed for a U.S. IPO, with IPOX® CEO Josef Schuster telling Reuters the deal could help reopen the U.S. market for larger China-based issuers.