SchusterWatch #848 (6/29/2026)

Choppy Markets: Most IPOX® Indexes fell in post-expiration trading last week.

Target Market for M&A: IPOX® 100 U.S. has 2nd stock acquired in three weeks.

Big Movers: APGE, MANE, CGON, LLY, RVMD, SPCX, CRWV, VIK, LTM, ARM.

IPOs: Doncaster jumps, poor SpaceX showing pressures OpenAI IPO schedule.

WEEKLY OVERVIEW: Post-expiration and ahead of the shortened U.S. quarter-end trading week, equities traded mostly lower, weighed down by profit-taking in the global AI and semiconductor trade and big weakness across Asia-Pacific, particularly China. U.S. yields fell, with the market seemingly encouraged by the stance of the new Fed chair toward fighting inflation.

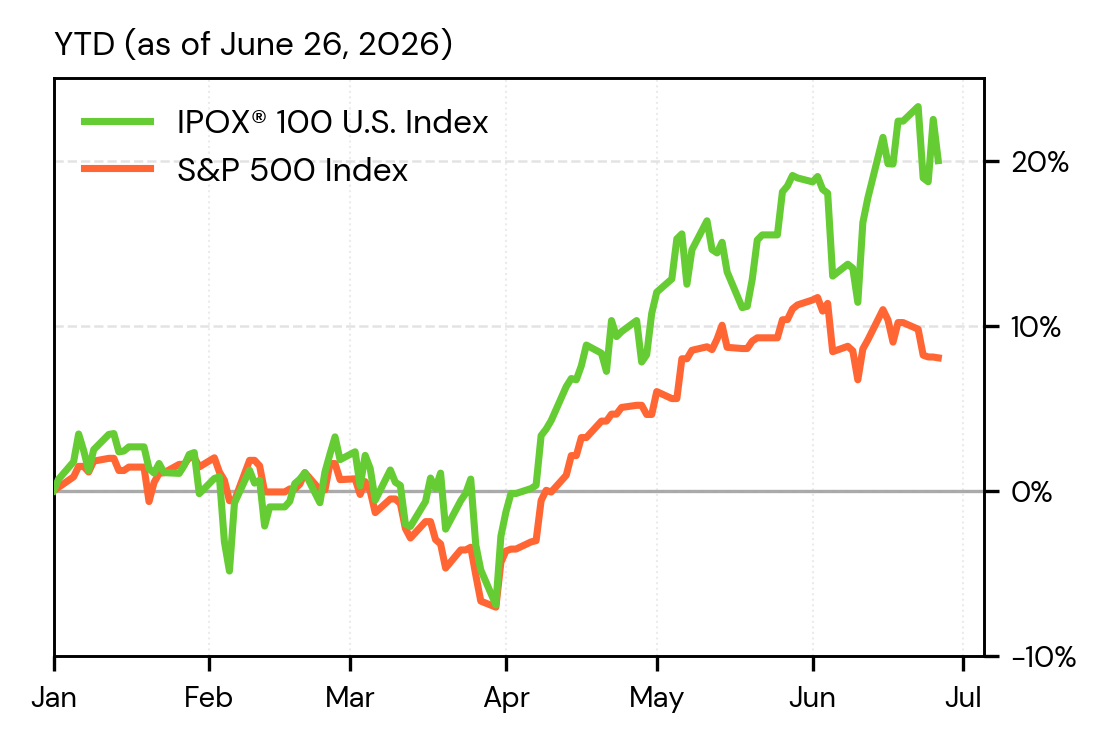

UNITED STATES: The IPOX® 100 U.S. Index (IPXO), key U.S. innovation gauge tracked by the First Trust U.S. Equity Opportunities ETF (Ticker: FPX), declined by -1.97% to +19.90% YTD last week, just 2 bps shy of the performance of the S&P 500 (SPX), the benchmark for U.S. stocks, while outperforming the tech-heavy Nasdaq 100 (NDX) by a large +226 bps. 60% of portfolio holdings rose, with the average (median) equally weighted stock adding +2.22% (+3.52%), massively better than the applied market-cap-weighted index and underscoring the big impact of profit-taking among our largest holdings into quarter-end. After the buyout of biotech Nuvalent (NUVL), biotech Apogee Therapeutics (APGE US: +46.66%) became the second IPOX® 100 U.S. (ETF: FPX) portfolio holding to be acquired at a big premium by large pharma within the past three weeks, underscoring the attractiveness of the IPOX® 100 U.S. (ETF: FPX) as a target market for corporate M&A. Amid the big rotation into health care stocks, other notable movers included biotechs VeraDermics (MANU US: +35.18%), CG Oncology (CGON US: +17.81%), and newly added IPO M&A plays Eli Lilly (LLY US: +9.97%) and most promising superstar Revolution Medicines (RVMD US: +11.71%). Profit-taking weighed on everything AI and Space, with a focus on weak low-float SpaceX (SPCX US: -17.17%) and CoreWeave (CRWV US: -18.12%).

Year-to-Date Performance of the IPOX® 100 U.S. Index

INTERNATIONAL: After the big run-up into expiration, the IPOX® International Index (IPXI), tracked by the First Trust International Equity Opportunities ETF (Ticker: FPXI), declined by -4.37% to +36.15% YTD last week. Strength in travel stocks, including cruise line operator Viking Holdings (VIK US: +6.27%) and Latin American Airlines (LTM US: +5.16%) on lower crude oil, was unable to offset the declines in some of the tech heavyweights, including Arm Holdings (ARM US: -23.94%), Kioxia (285A JP: -15.12%), and Technoprobe (TPRO IM: -11.89%), while renewed uncertainties over the size of European military spending pressured global defense stocks, including South Korean shipbuilder HD Hyundai Heavy Industries (329180 KS: -15.44%).

THE IPOX® SPAC INDEX: The Index declined -1.96% last week, reducing year-to-date performance gains to +16.25%. Oilfield services provider National Energy Services Reunited (NESR US: +15.08%) was the best performer, benefitting from renewed strength in energy services demand. Rocket Lab (RKLB US: -21.17%) was the worst performer as space-related equities came under broad pressure across the sector. Three SPACs announced merger targets during the week, including Churchill Capital XI (CCXI US), which agreed to combine with Agility Robotics. OTC-traded TLGY Acquisition completed its business combination with StablecoinX (USDE US), and the combined entity successfully moved its listing to the Nasdaq. Four new SPAC IPOs launched in the U.S. during the week.

ECM REVIEW: 27 companies went public globally last week, raising $5.95 billion. New listings gained an average of +88.00% from offer price to Friday’s close (median: +3.94%). U.S. deal flow was led by British aircraft engine partmaker Doncasters (DPC US: +42.06%, $919 million offer), Mexico silver explorer Sinda (SIND US: unch, $213 million), and Chinese car dealer software firm DSC (DSC US: -46.71%, $51 million). Hong Kong issuance saw electronics manufacturer Lingyi iTech (1688 HK: -4.62%, $1.05 billion), chipmakers SG Micro (3661 HK: +47.07%, $587 million) and CFMEE (9630 HK: +103.77%, $414 million), Indonesian gold miner Merdeka Gold (6228 HK: -6.54%, $304 million), battery part maker Senior Technology Material (6067 HK: +1.67%, $171 million), and pharma HJ Science (6132 HK: -46.11%, $142 million). Smaller IPOs delivered outsized returns, including parking operator Keytop (2272 HK: +203.92%), visual AI firm HQVT (1392 HK: +158.19%), Micot Pharma (2335 HK: +117.14%), and analytics firm WengeAI (1956 HK: +84.02%).

U.S. IPOs lead this week’s pipeline with Italian digital business acquirer Bending Spoons (BSP US, $1.6 billion) and micromobility network Lime (LIME US, $174 million). Hong Kong remains busy with consumer electronics maker Anker (668 HK, $591 million), data center connectivity firm Crealights (1191 HK, $195 million), kidney pharma Alebund (9637 HK, $164 million), caviar producer Xunlong Sci-Tech (6715 HK, $157 million), robotic part maker Laifual Drive (3952 HK, $147 million), InsurTech Baige Online Digital (2672 HK, $66 million), surgical robotics firm True Health Medical (2697 HK, $62 million), and tetanus vaccine producer Jiangxi Institute of Biological Products (6915 HK, $60 million). South Korea’s KOSDAQ is set to add automotive AI vision perception software firm STRADVISION (475040 KS, $57 million).