SchusterWatch #847 (6/22/2026)

AI Surge: IPOX® Indexes soar as storage, semis, electrification lead.

Historic Close: FPX tops $200 for first time; IPOX U.S. Index gains +4.14%.

Movers: GEV, CoreWeave, DoorDash, Kioxia Seagate, Knowledge Atlas, ARM.

IPOs: Hong Kong dominates calendar; Doncasters sole sizable U.S. deal.

WEEKLY OVERVIEW: Equity markets rose during the shortened U.S. Expiration/Fed week, as risk declined (VIX: -5.09%) and the IPOX® Indexes remained major beneficiaries of the big AI trade favoring storage device firms, semiconductors, and electrification. Gains across IPOX® continued to be driven by a series of portfolio holdings largely absent from traditional benchmarks, highlighting the advantage of capturing New Listings and related corporate actions as a separately tradable equity sector.

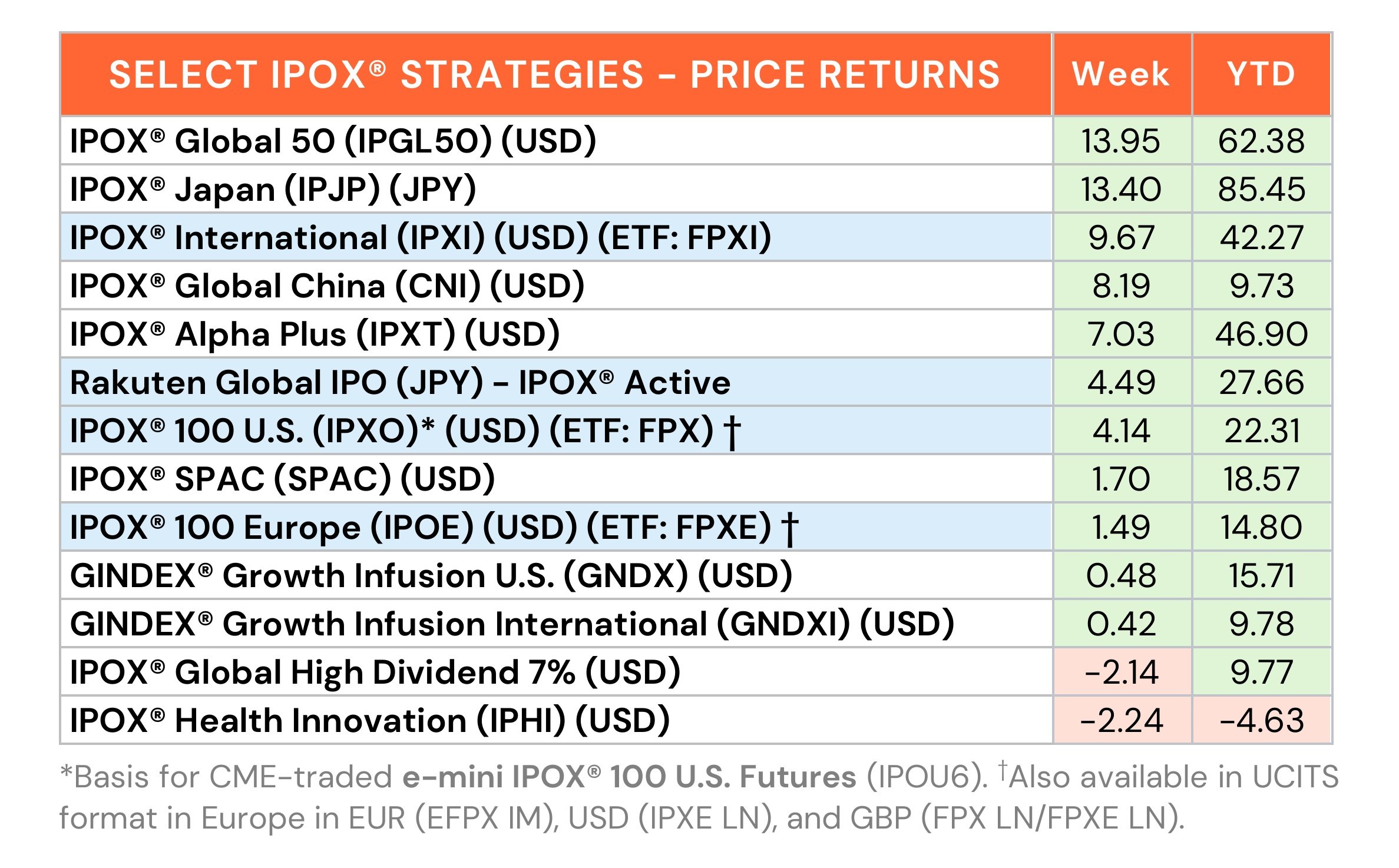

UNITED STATES: The IPOX® 100 U.S. Index (IPXO), tracked by the First Trust U.S. Equity Opportunities ETF (Ticker: FPX), advanced +4.14% last week, outperforming the S&P 500 (SPX), the benchmark for U.S. stocks, by +321 bps and the Nasdaq 100 (NDX) by +154 bps. The FPX ETF closed above $200 for the first time in history after launching at $20 in 2006, underscoring the long-term value creation captured by the IPOX® methodology. Big gains in AI-related exposure drove the jump, led by energy spin-off GE Vernova (GEV US: +17.97%), AI cluster provider CoreWeave (CRWV US: +17.30%), food delivery firm DoorDash (DASH US: +15.19%), data storage device maker Seagate Technology (STX US: +14.95%), and newly added SpaceX (SPCX US: +14.94%). While SpaceX provided another strong early-week boost, we note that the stock may trade more rangebound as investors monitor potential debt-market activity.

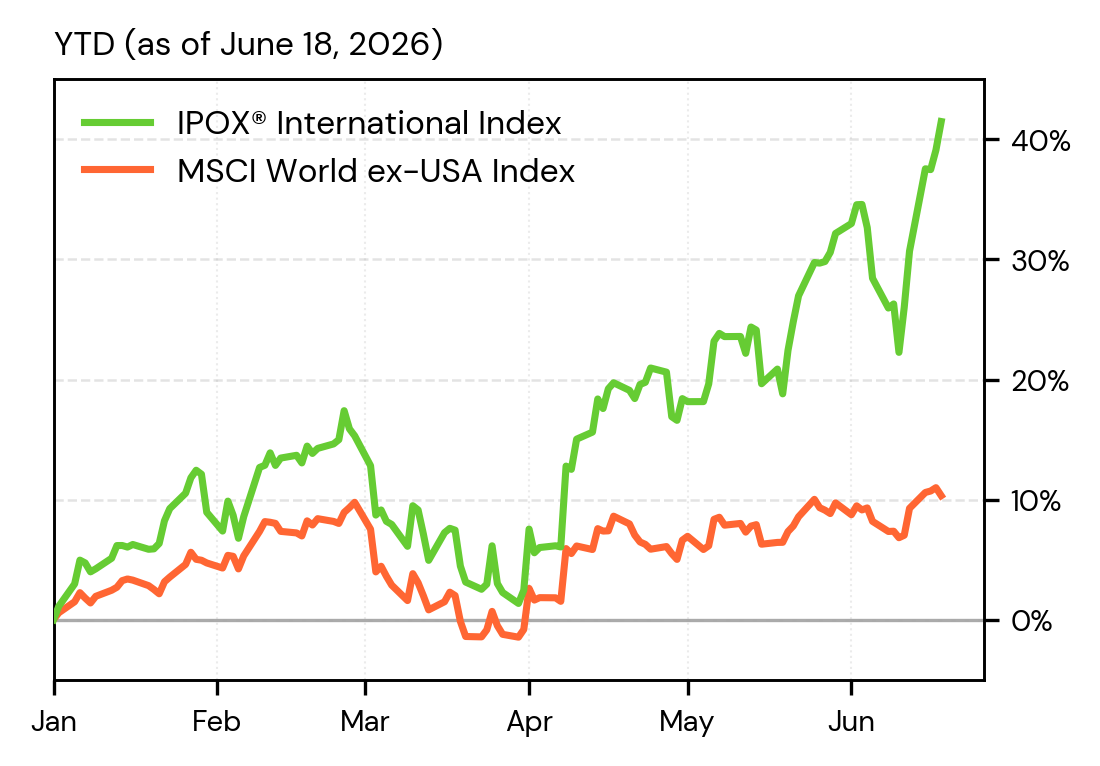

INTERNATIONAL: The IPOX® International Index (IPXI), tracked by the First Trust International Equity Opportunities ETF (Ticker: FPXI), soared +9.67% last week, as Asia-Pacific technology exposure rallied on major upgrades, led by Chinese AI lab Knowledge Atlas (2513 HK: +90.88%) after emerging as JPMorgan top-pick. The moves in tech also powered the IPOX® Global 50 (IPGL50: +13.95%) and IPOX® Japan (IPJP: +13.40%), with huge gains in benchmark-light AI and semiconductor exposure included Chinese semiconductor firm GigaDevice (3986 HK: +43.69%), Japanese memory chipmaker Kioxia (285A JT: +33.74%), Taiwanese electronic components and semiconductor play Yageo (2327 TT: +26.32%), and Chinese GPU/semiconductor firm Shanghai Iluvatar CoreX (9903 HK: +19.32%). The IPOX® 100 Europe (IPOE), tracked by FPXE, added +1.49%, buoyed by British chipmaker ARM Holdings (ARM US: +15.40%), Swiss gas-engine maker Accelleron (ACLN SE: +13.36%), and Italian semis testing firm Technoprobe (TPRO IM: +12.88%).

YTD Performance of the IPOX® International Index (ETF: FPXI):

THE IPOX® SPAC INDEX: Last week, the IPOX® SPAC Index, featured in Reuters coverage on the SPAC revival, gained +1.70%, bringing year-to-date performance gains to +18.57%. Cryptocurrency mining and data center operator Cipher Mining (CIFR US: +19.10%) was the best performer as shares continued to benefit from strong momentum and the company's ongoing expansion of its data center operations. Geolocation services provider NextNav (NN US: -15.44%) was the worst performer after announcing the redemption of its senior secured convertible notes and recent profit-taking. One SPAC announced a merger target, with Silicon Valley Acquisition (SVAQ US) agreeing to combine with quantum firm EigenQ. Live Oak Acquisition V (LOKV US) completed its business combination with Teamshares, an acquirer of small business ownership transitions, with the first trading day of the combined company yet to be announced. 4 new SPAC IPOs launched in the U.S. during the shortened trading week.

ECM REVIEW: 19 companies went public globally last week, raising $1.5 billion. New listings gained an average of +44.73% from offer price to Friday’s close (median: +37.50%). Sizable deal flow was led by Japanese ride-hailing app GO Inc. (581A JP: -4.25%, $560 million), followed by U.S. cardiovascular biotech Kardigan (KARD US: +37.50%, $400 million) and Chinese sensor chip maker SENASIC Electronics Technology (6675 HK: +81.92%, $125 million). Other notable listings included Norwegian furniture retailer Bohus (BOHUS NO: +12.90%, $98 million), regional bank First Carolina Financial Services (FCBM US: +0.80%, $69 million), and Chinese plum drink maker Liuliumei (6658 HK: +216.20%, $64 million), which drove the big average aftermarket return. U.S. nuclear energy firm Deep Fission (FISN US: -9.00%, $40 million) lagged.

During this week’s global IPO calendar, the only sizable U.S. listing scheduled is British aerospace precision cast components maker Doncasters (DPC US: $700 million), discussed by IPOX® Associate Lukas Muehlbauer in Reuters coverage. The rest of the week is dominated by deal flow in Hong Kong, led by electronics manufacturing and hardware solutions provider Lingyi iTech (1688 HK: $1.05 billion), analog IC and sensor designer SG Micro (3661 HK: $587 million), lithography equipment maker CFMEE (9630 HK: $414 million), Indonesian gold miner Merdeka Gold (6228 HK: $304 million), lithium-ion battery separator maker Senior Technology Material (6067 HK: $171 million), and metabolic peptide-drug developer Micot Pharma (2335 HK: $156 million), among others.