SchusterWatch #845 (6/8/2026)

Risk Off: Equities fall ahead of SpaceX IPO. IPOX® Indexes lead decline.

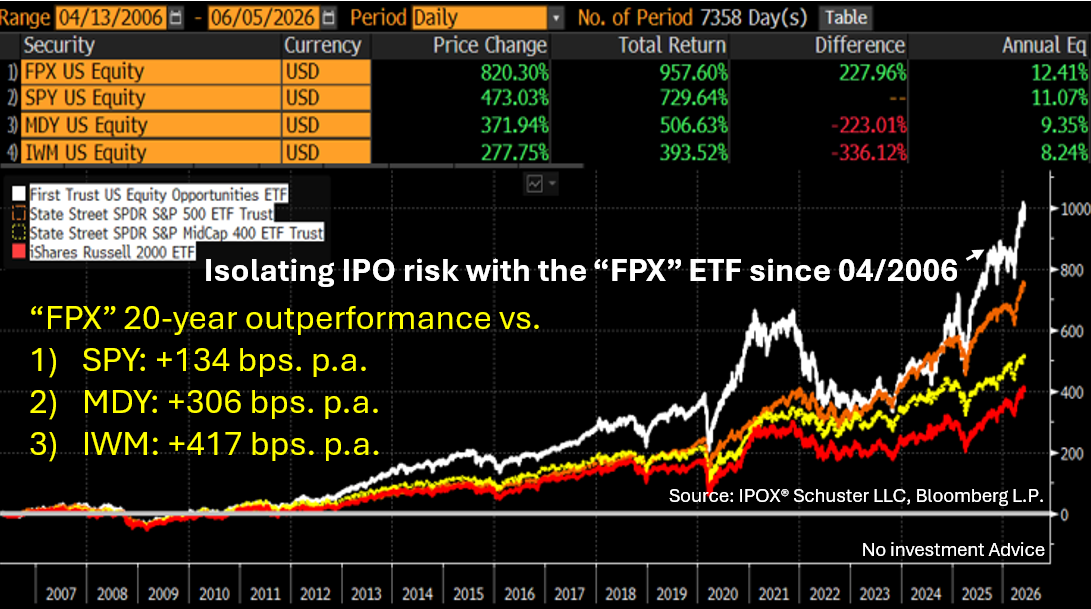

A Novel Approach: Isolating SpaceX’s IPO risk with the IPOX® 100-linked “FPX”.

Big Movers: MMED, PL, CRLC, PAYP, 9903 HK, 2513 HK, CSG NA.

IPOs: SpaceX meets fully priced IPOs, as Cerebras returns to near IPO price.

WEEKLY OVERVIEW: Equity Markets fell sharply ahead of the start of June Futures Roll, as good U.S. unemployment numbers cooled interest rate cut hopes and big profit-taking in high-beta names around everything AI and crypto, ahead of the landmark SpaceX (SPCX) IPO on Friday, June 12, spilled over into broad-based U.S. equity weakness, while risk spiked (VIX: +40.41%).

OUR NOVEL APPROACH TO SPACEX: Our investment philosophy is to pool New Listings into a separately tradable equity sector because the ‘going public’ effects are real and truly unique to IPOs. This approach has helped us to isolate the unique IPO risk, while capturing the opportunities of the New Listings market.

UNITED STATES: The IPOX® 100 U.S. Index (IPXO), tracked by the First Trust U.S. Equity Opportunities ETF (Ticker: FPX), reversed the previous week’s gains to shed -5.00% to +12.72% YTD, lagging the S&P 500 (SPX), the benchmark for U.S. stocks, by -241 bps last week. 64% of firms fell, with the average (median) equally weighted stock declining by -3.26% (-1.87%), reversing last week’s lag and underscoring the impact of profit-taking among heavyweights. SpaceX proxy trades Planet Labs (PL US: -37.00%) and AST Space (ASTS US: -17.47%), as well as fintech Circle Internet (CRCL US: -28.96%), fell most. As recent IPO chipmaker Cerebras (CBRS: -15.19%) deflates toward its $185 IPO price, we note another week of post-IPO losses for IL-based medical products distributor Medline (MDLN US: -8.07%), last year’s biggest U.S. deal. The stock is now closing in on its IPO price amid an FDA warning over contamination incidents in its production facilities.

INTERNATIONAL: The IPOX® International Index (IPXI), tracked by the First Trust International Equity Opportunities ETF (Ticker: FPXI), declined by -2.85% to +27.55% YTD last week, lagging its benchmark by -142 bps. Friday’s big profit-taking across China-linked AI exposure and weak global miners drove the declines, including Knowledge Atlas (2513 HK: -18.68%), Shanghai Iluvatar Core Semi (9903 HK: -18.08%) and spin-off Valterra Platinum (VALT LN: -14.45%). Some Nordic exposure had a standout week, with Norway’s oil producer Var Energy (VAR NO: +7.90%) leading the way, while Swedish wealth management platform Nordnet (SAVE SS: +5.57%) closed toward its best level ever. IPOX® also counted SoftBank-backed Japanese payment processor PayPay (PAYP US: -22.75%) as another recently issued large IPO displaying weak post-IPO stock market performance.

THE IPOX® SPAC INDEX: The Index fell sharply by -10.13% last week to +15.54% YTD. Geolocation services provider NextNav (NN US: +4.75%) rose by the most, while eye-disease biotech Oculis (OCS US: -51.22%) fell the most after its late-stage eye-disease trial failed to meet its primary endpoint. Three SPACs announced merger targets, including Titan Acquisition Corp (TACH US) with financial infrastructure platform OpenPayd. No SPACs completed business combinations during the week. Six new SPAC IPOs launched in the U.S. market.

ECM REVIEW: 16 firms went public globally last week, raising $7.1 billion. New listings gained an average of +58.11% from offer price to Friday’s close (median: +0.33%). The largest deal was gas engine maker Innio (INIO US: +23.33%), which raised $2.79 billion, followed by Honeywell-backed quantum computing firm Quantinuum (QNT US: +0.63%, $1.68 billion). Reuters featured IPOX® Associate Lukas Muehlbauer on Innio’s debut and AI infrastructure power demand, while IPOX® VP Kat Liu was cited on Quantinuum’s long-term opportunity across AI, communications, cybersecurity and security.

Other notable deals included defense contractor Applied Aerospace & Defense (AADX US: -7.00%, $650 million), mobile advertising specialist Liftoff Mobile (LFTO US: +23.70%, $437 million), and materials firm Sunshine Silver Mining & Refining (SSMR US: +27.04%, $270 million). Hong Kong deals included wind energy firm Dajin Heavy Industry (1081 HK: +0.00%, $848 million), biologics pharma company LongBio (1779 HK: +37.21%, $174 million), drugstore retailer Lung Fung Group (2290 HK: -45.75%, $83 million), and renewable energy biotech LanzaTech Technology (2553 HK: +107.81%, $75 million).

HISTORICAL WEEK AHEAD: Friday, June 12, will see the SpaceX (SPCX US) IPO, with the firm planning to sell ca. 4% for $75 billion, marking the largest-ever IPO, but also the arrival of an extremely low-float deal onto the market. Other IPOs include modular gas power systems provider ERock (EROC US, $600 million), engineered peptide therapy developer Parabilis Medicines (PBLS US, $450 million), and digital-first sustainable bank Forbright (FRBT US, $150 million). Outside the U.S., Danish technical installation services provider InstallatørGruppen (IG DC, $163 million), Swedish investment group Tången Industrikapital (TANGENB SS, $111 million), and South Korean fashion chain Piece Peace Studio (0117P0 KS, $33 million) are lined up.