SchusterWatch #842 (5/18/2026)

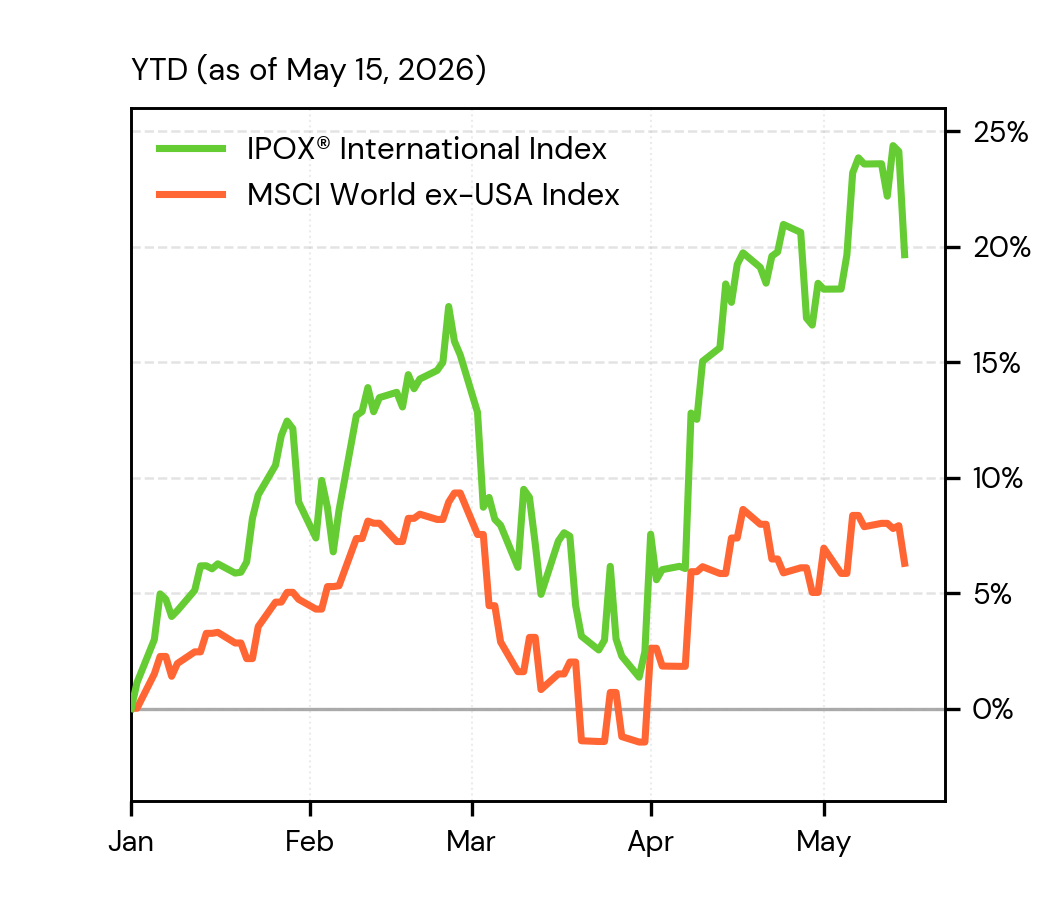

Profit Taking and Yields pressure: IPOX® Indexes consolidate after surge.

A New Generation of Growth: Select Info Tech ex U.S. soars last week.

>20% Movers: Europe’s/ Italy’s Technoprobe is the New Kid on the Block.

IPO Action: Cerebras opens hot, finished week cold. APAC IPOs in focus.

WEEKLY OVERVIEW: The market played catch-up with the previous week’s strongly positive earnings-driven momentum across most IPOX® Indexes through Thursday of last week’s U.S. options expiration week. Toward the weekend, a big spike in U.S. yields, with the long end closing above the key 5% mark, inflicted damage across U.S. equities, while risk rose (VIX: +7.21%).

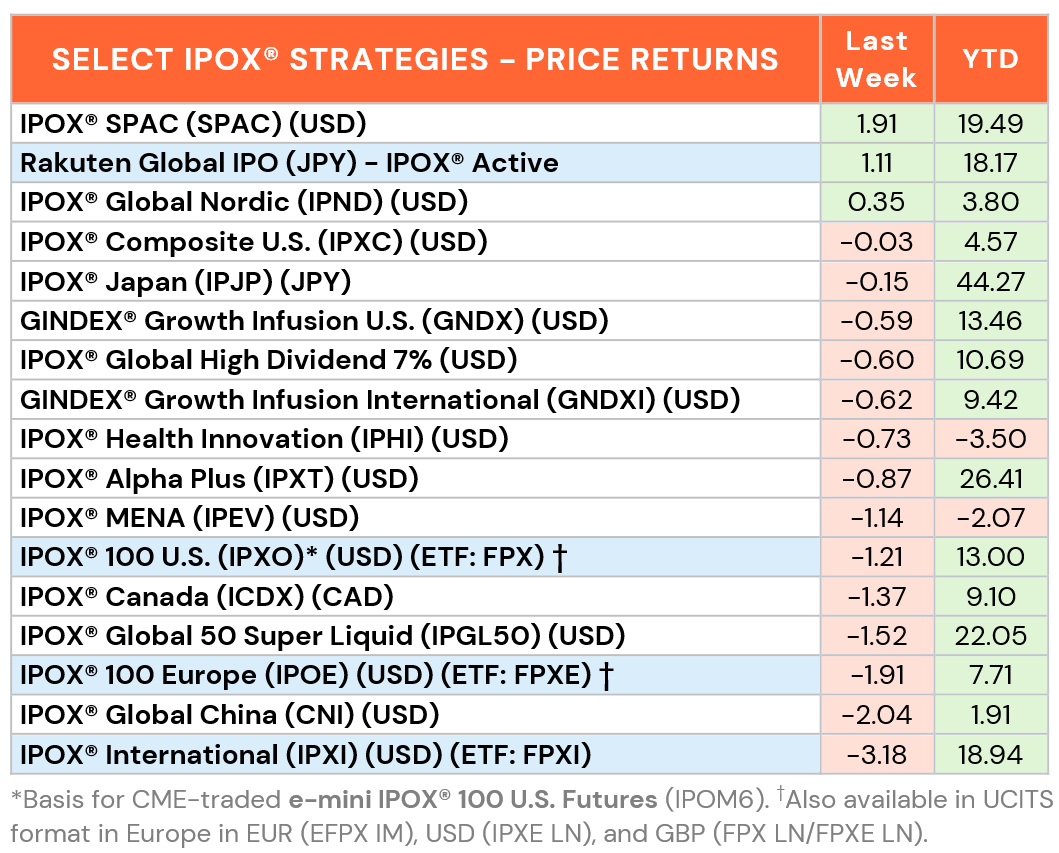

UNITED STATES: The IPOX® 100 U.S. (IPXO), underlying index for the First Trust U.S. Equity Opportunities ETF (ticker: FPX), fell -1.21% to +13.00% YTD, lagging the benchmark S&P 500 (SPX) by 134 bps last week. 61/100 portfolio holdings fell, with the average (median) equally weighted stock declining by -0.97% (-1.63%), broadly in line with the applied market-cap-weighted index. Positive momentum decelerated notably during the week amid the absence of catalysts to drive prices higher after what has been an excellent earnings season. Upside movers that stood out continued to include takeover candidate and coconut water maker The Vita Coco Co. (COCO US: +9.55%), while Honeywell spin-offs Solstice (SOLS US: +8.77%) and Qnity Electronics (Q US: +6.72%) excelled again, and de-SPAC telecom AST SpaceMobile (ASTS US: +11.49%) continued to trade as a best-in-class SpaceX proxy. Negative post-earnings momentum eroded more of the post-IPO gains in healthcare holding 12/2025 IPO Medline (MDLN US: -8.43%), last year’s largest and most significant U.S. IPO.

A New Generation of Growth – Captured as a Group in the IPOX® International ETF (FPXI): As investors seek to broaden their exposure to technology and related growth sectors beyond the key names in the U.S., they often find excellent diversification opportunities in non-U.S. domiciled firms trading in a wide post-IPO window, or in firms that have pursued the buyout of an IPO company (“IPO M&A”) and trade in the U.S. or on a foreign market. Here, last week’s breakout in Italy’s chip-testing machine maker Technoprobe (TPRO IM: +30.40%) comes as no surprise after the firm recorded another massive earnings beat, which brought the company one step closer to being categorized as a much-sought-after European tech champion. Select other portfolio holdings recording big gains included Taiwan’s electronic components makers Yageo (2327 TT: +17.10%) and WT Microelectronics (3036 TT: +12.27%), as well as China-domiciled key AI play Knowledge Atlas Technology (2513 HK: +12.68%) and semiconductor maker GigaDevice (3986 HK: +11.02%), both recent IPOs in the Hong Kong market. Canada-domiciled firms from the growth segments of the energy and basic materials sectors also stood out, including high-dividend-paying new listings energy infrastructure play South Bow (SOBU US: +7.40%) and oil and natural gas explorer Whitecap Resources (WCP CN: +7.10%). Some consumer-related exposure in the portfolio declined strongly last week, with a focus on Canada’s online fashion portal Group Dynamite (GRGD CN: -16.40%), Chinese/Finnish high-end sportswear maker Amer Sports (AS US: -8.85%), and airline operator LATAM Airlines (LTM US: -8.33%).

THE IPOX® SPAC INDEX: The Index gained +1.91% last week, bringing YTD performance to +19.49%. LiDAR sensor manufacturer Ouster (OUST US: +38.33%) surged after reporting sensor compatibility with NVIDIA’s autonomous driving reference platform, helping accelerate autonomous vehicle deployment. Weapon detection screening company Evolv Technologies (EVLV US: -19.15%) tanked following Q1 earnings and weaker guidance. Quartzsea Acquisition (QSEA US) announced a merger with disposable plastic container supplier Eight Direction Technology. Boost Run (BRUN US), an NVIDIA-preferred Cloud Provider, completed its merger with Willow Lane Acquisition. 6 new SPAC IPOs launched in the U.S.

ECM REVIEW: 23 firms went public globally last week, raising $11.28 billion. New listings surged by an average +130.75% from offer price to Friday’s close (Median: +26.27%). The standout deal was AI chipmaker Cerebras Systems (CBRS US: +51.20%), which raised $6.38 billion in the largest IPO globally YTD. Geothermal energy developer Fervo Energy (FRVO US: +52.07%) followed with a $2.17 billion raise, adding to enthusiasm around alternative energy infrastructure. Outside the U.S., sovereign wealth vehicle National Investment Fund of the Republic of Uzbekistan (UZNF LI: +10.00%) raised $586 million in London, while Hong Kong saw AI drug developer Metis TechBio (7666 HK: +106.67%), oncology-focused IMPACT Therapeutics (7630 HK: +99.20%), and robotics company Shenzhen Ldrobot (1236 HK: +74.81%). U.S. emergency services provider GMR Solutions (GMRS US: -10.87%) was among the weaker performers. We also note EagleRock Land (EROK US: +16.49%), which raised $320 million, with IPOX® Associate Lukas Muehlbauer commenting in Reuters coverage. This week, Chicago-based investment banking advisory firm Lincoln International (LCLN US, $400M) headlines issuance. Hong Kong listings include industrial robotics firm Robotphoenix Intelligent Technology (6871 HK, $96M), autonomous driving firm UISEE Technologies (1511 HK, $111M), and CNC equipment maker Shanghai Top Numerical Control Technology (7688 HK, $220M). Korea’s MakinaRocks (477850 KS, $26M) is expected to test investor appetite for industrial AI software, while biotech TenNor Therapeutics (6872 HK, $80M) adds to the recent momentum in healthcare-linked new issuance.