SchusterWatch #839 (4/27/2026)

Fresh Records For Multiple IPOX® Indexes: AI and Alternative Energy lead.

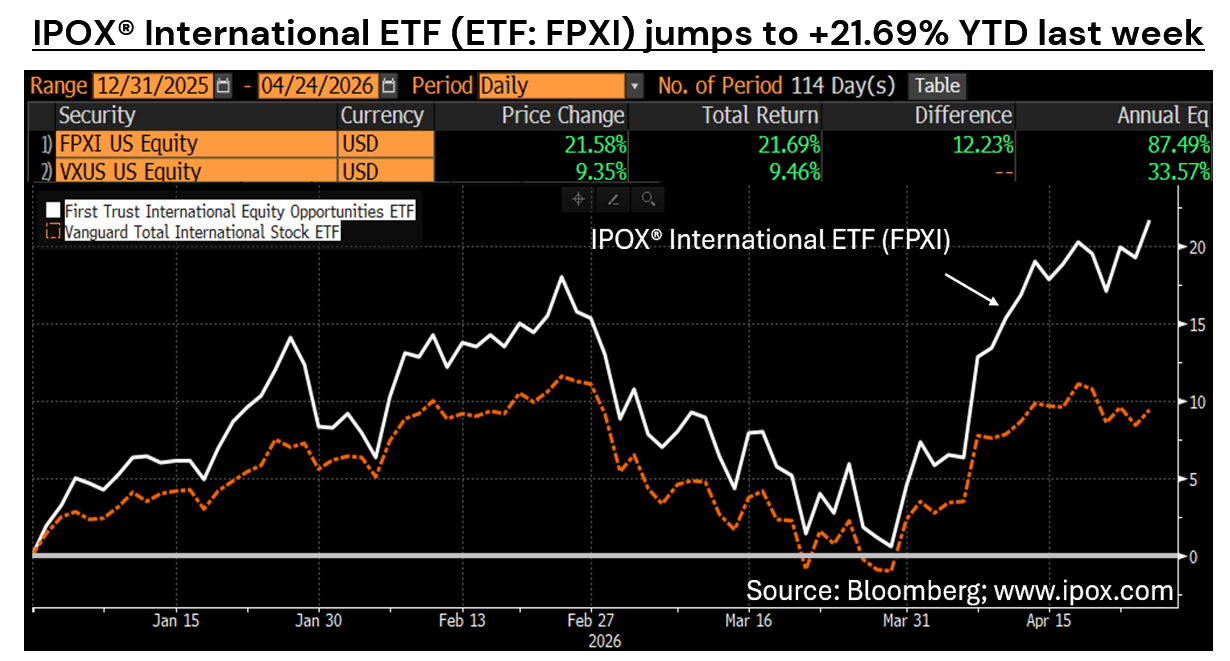

+371 bps. Weekly Beat: IPOX® International (ETF: FPXI) soars to 21% YTD.

>20% Movers: Credo Technology, ARM Holdings, HD Hyundai Heavy.

Strong IPO Momentum, Deals Lined Up: PS, AVLN, SBMT, 1879 HK.

OVERVIEW: Select IPOX® Indexes rose for a 4th week, as an overweight to AI- and Electrification mitigated the negative impact from weak China as well as declines in U.S. healthcare and a renewed slump in software-related stocks. With Geopolitics driving Crude Oil prices higher and relative weakness in Markets abroad, equity risk rose (VIX: +7.04%) with U.S. yields.

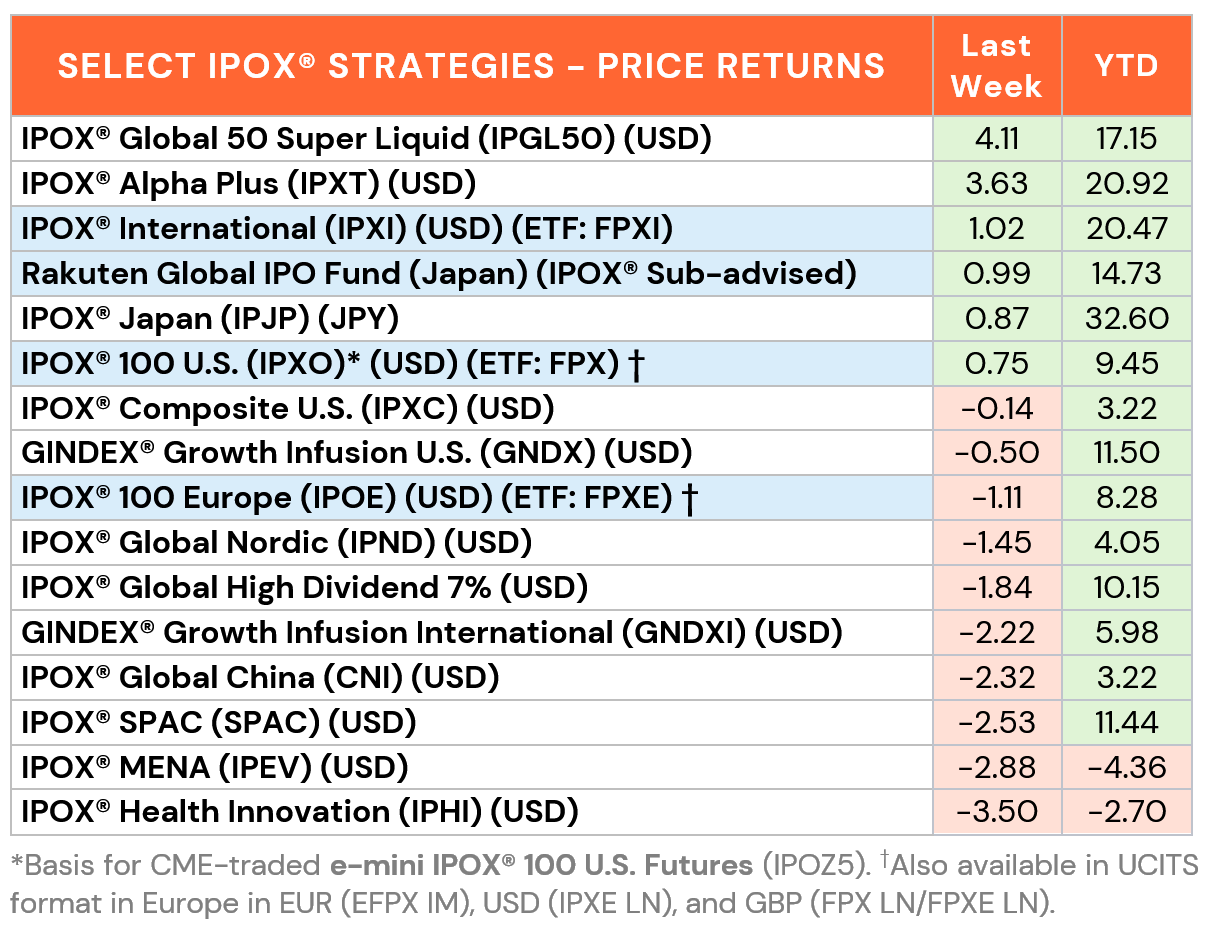

UNITED STATES: With 29% of its market cap reporting on earnings this week, the IPOX® 100 U.S. (ETF: FPX) - gold standard for U.S. IPOs- added +0.75% to +9.45% YTD, closing out the week at a fresh all-time high and +20 bps. ahead of benchmark S&P 500 (SPX). 40% of firms rose, with the average (median) equally weighted stock shedding -1.10% (-1.30%), strongly lagging the applied market-cap weighted IPOX® 100 U.S. Big gains in the IPOX® heavyweights including Electrification leader GE Vernova (GEV US: +14.60%) after big earnings and memory devices maker Sandisk (SNDK US: +7.48%) more than offset declines amongst many other portfolio holdings, some earnings driven, such as defense play Karman (KRMN US: -15.98%), Figure Technology Solutions (FIGR US: -12.33%) and MiniMed (MMED US: -8.59%). We note another big week for the IPOX® Alpha Plus (IPXT), an actively managed IPOX® Strategy which takes a global perspective to U.S. deal flow. The strategy soared +3.63% to +20.92% YTD.

INTERNATIONAL/GLOBAL: Similar to the U.S., Markets, abroad traded highly uneven last week. While the IPOX® Global China (CNI: -2.32%) and IPOX® MENA (IPEV: -2.22%) fell, an overweight to AI and select specialty stocks related to defense and personal healthcare benefited select IPOX® Strategies. Here, big relative strength in the IPOX® 100 Europe (IPOE: -1.11%, ETF: FPXE) and IPOX® Japan (IPJP: +0.87%) drove the IPOX® International (IPXI: +1.02%) and IPOX® Global 50 Super Liquid (IPGL50: +4.11%) significantly higher. Amid the global frenzy into semiconductor stocks, Britain-based ARM (ARM US: +40.83%), Koreas top defense play HD Hyundai Heavy Industries (329180 KS: +30.54%), Japan’s buoyed memory chip maker Kioxia (285A: +13.27%), Germany’s Siemens Energy (ENR GY: +9.04%) and Koreas personal care firm APR (278470 KS: +7.27%) led the way. In what was a big rotation trade out of miners and health care/biotech last week, Valterra Platinum (VALT LN: -15.71%), Canada’s DP Metals (-8.64%), Hong Kong-listed Sichuan Kelun-Biotech Biopharma (6990 HK: -8.12%) and Canada’s Triple Flag Precious Metals (TFPM US: -7.15%) ranked towards the bottom of last week’s IPOX® Performance Ranking.

THE IPOX® SPAC INDEX: The index declined by -2.53% to +11.44% last week. LiDAR technology and traffic management company Ouster (OUST US: +16.32%) was the best performer after securing a traffic signal deployment in the Greater Atlanta area, while wireless spectrum and geolocation services provider NextNav (NN US: 22.43%) declined by the most after regulatory scrutiny. Three SPACs announced merger targets, including Archimedes Tech SPAC Partners II (ATII US) with U.S.-based battery cell manufacturer Forge Nano. No SPACs completed mergers and no new SPAC IPOs launched in the U.S. during the week. In deSPAC M&A, 2019 deSPAC payment processor Repay Holdings (RPAY US) is reviewing a take-private proposal from its largest shareholder Forager Capital.

ECM REVIEW: Global markets remained highly active last week, with 24 firms raising $6.6 billion and new listings posting an average gain of +33.80% (Median: +21.06%) from offer size to Friday’s close. In the U.S., we recorded three notable deals: Amazon-backed modular nuclear reactor developer X-Energy (XE US) raised over $1 billion, gaining +26.96%. The firm was joined by convenience store operator Yesway (YSWY US: +8.75%, $280 million) and defense-adjacent materials firm Elmet Group (ELMT US: +21.43%, $138 million). Hong Kong saw its largest listing YTD with circuit board maker Victory Giant Technology (2476 HK: +50.37%) raising $2.95 billion, while smartphone maker Huaqin (3296 HK) gained +14.22% on a $581 million raise. IPO activity this week is led by alternative asset manager Pershing Square (PS US), targeting a massive $5 billion debut. Other deals include respiratory biotech Avalyn Pharma (AVLN US, $200 million) and minerals explorer Silver Bow Mining (SBMT US, $50 million). IPOX® CEO Josef Schuster underlined the potential of the IPO asset class in Reuters, highlighting that “a golden age for U.S. IPOs has arrived”. In Hong Kong, expected debuts include optoelectronic computing firm Xizhi Tech (1879 HK, $323 million), biologic drugmaker Mabwell (2493 HK, $185 million), and commercial IoT provider Sunmi Technology (6810 HK, $135 million). Additional listings include South Korean EV charging solutions provider Chaevi (0011T0 KS, $105 million) and German electronics firm Electrovac (EVAC GR, $50 million).