SchusterWatch #838 (4/20/2026)

IPOX® Indexes extend big surge to close at to fresh records; High Beta leads.

IPOX® SPAC and IPOX® Alpha Plus soar 8%-10% as Innovation trumps anew.

>20% Movers: NextNav, Dave, Shanghai Iluvatar, GigaDevice, Pfisterer.

IPO Boom as deals debut well: XE, NHP, YSWY and ELMT lined up.

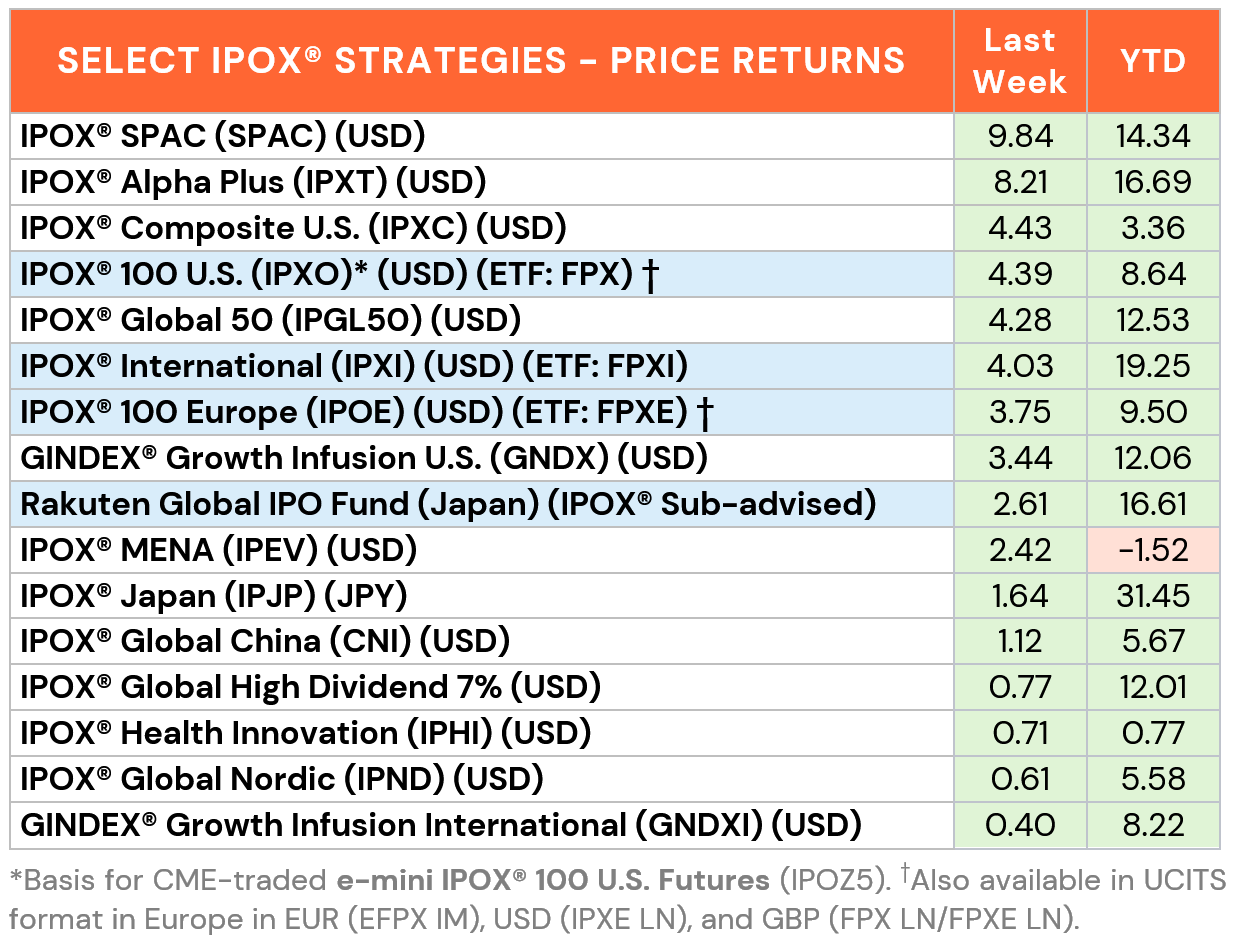

OVERVIEW: The IPOX® Indexes surged for a 2nd week across the board with select Strategies closing out Friday at fresh All-Time Highs. As the broad benchmarks played catch up to the previous week’s big IPOX® Strength, most relative upside was recorded in our Alpha-focused Strategies, such as the IPOX® SPAC (SPAC: +9.84%) and IPOX® Alpha Plus (IPXT: +8.21%). More Geopolitical appeasement pressured risk anew (VIX: -9.09%), while U.S. rates fell on hopes of muted inflation.

UNITED STATES: Ahead of key earnings, the IPOX® 100 U.S. ETF (FPX) rallied +4.39% to +8.64% YTD to close at a fresh weekly All-Time High, -15 bps. shy of last week’s return of the S&P 500 (ETF: FPX). 82% of portfolio holdings rose with the average (median) equally weighted firm adding +5.83% (+3.69%), +114 bps. better than when compared to the applied market cap weighted index. De-SPACs geolocation tech solutions provider NextNav (NN US: +49.41%) and fintech Dave (DAVE US: +35.22%) ranked as the top performing stocks in the “FPX” ETF last week, while Materials and Energy exposure lagged.

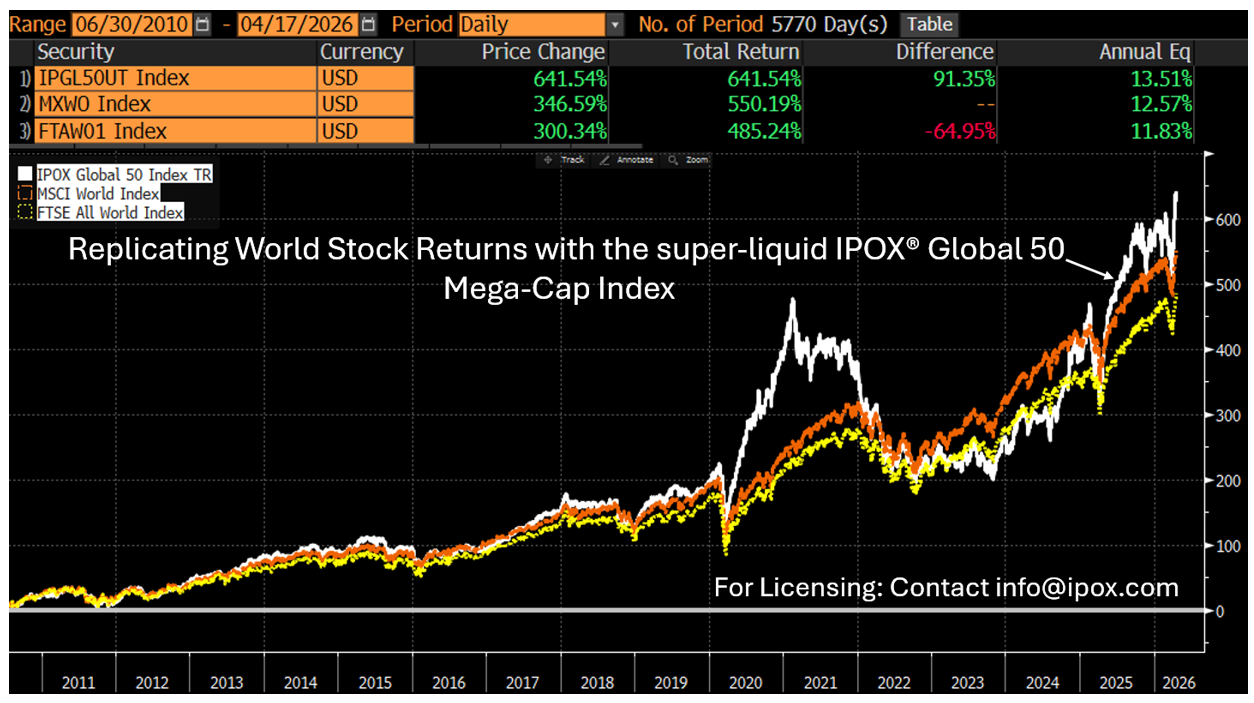

GLOBAL/INTERNATIONAL/EUROPE: Select IPOX® Strategies closed out the trading week at or near All-Time Highs as well. Top of the list ranked the super-liquid IPOX® Global 50 (IPGL50: +4.28%) benefiting from another big week for the IPOX® International (ETF: FPXI). Strong gains in European stocks exclusively listed in the U.S. drove the IPOX® 100 Europe (IPOE) to extend its YTD lead vs. the hard-to-beat STOXX 50 (SX5L) to ca. +400 bps. to close out the week at the highest level on record. Across APAC, the IPOX® Global China (CNI: +1.12%) lagged, while IPOX® Japan (IPJP: +1.64%) set a fresh record and the IPOX® MENA (IPEV) recovered more of its YTD losses.

THE IPOX® SPAC INDEX: The Index surged +9.84% to +14.34% YTD last week. Quantum computing firm IonQ (IONQ US: +60.09%) was the best performer after announcing a foundational technical milestone toward scaling commercial quantum computing. SpaceX proxy AST SpaceMobile (ASTS US: -9.87%) fell after Amazon’s deal with Globalstar and concerns in would intensify competition in the direct-to-cell market. Three SPACs announced merger targets during the week, such as Sizzle Acquisition II (SZZL US) which agreed to combine with Swiss-based steel trading and processing company Trasteel. No SPACs completed mergers. Four new SPAC IPOs launched in the U.S.

ECM DEALS: 21 firms went public globally, raising a sizable $7 billion last week, posting an average gain of +86.72% (Median: +48.57%). The U.S. led the way, anchored by the $2.57 billion offering from HVAC and data center ventilation firm Madison Air Solutions (MAIR US: +20.19%), the largest industrials IPO since 1999. Discussing the debut in Reuters, IPOX® VP Kat Liu noted a return of investor appetite for proven cash-generating businesses. The defense sector also saw heavy action, with parts supplier Arxis (ARXS US) gaining +35.71% on a $1.3 billion raise, alongside drone maker Aevex (AVEX US: +34.65%, $320m). In Nikkei, IPOX® CEO Josef Schuster highlighted that the defense IPO market remains robust and less affected by volatility. Biotech also delivered strong returns, with diet drug pharma Kailera Therapeutics (KLRA US) surging +62.50% on a $625 million raise. IPOX® Associate Lukas Muehlbauer told Reuters that Kailera's debut signals a potential biotech turnaround. Protein analysis device maker Alamar Biosciences (ALMR US: +29.41%, $191m) also gained. In Hong Kong, debuts skyrocketed, led by design software firm Manycore (68 HK: +144.09%, $156m), energy storage firm Sigenergy (6656 HK: +85.07%, $562m), and image sensor maker Gpixel (3277 HK: +75.53%, $332m).