SchusterWatch #835 (3/30/2026)

IPOX® Indexes track decline of benchmarks as war uncertainty takes toll.

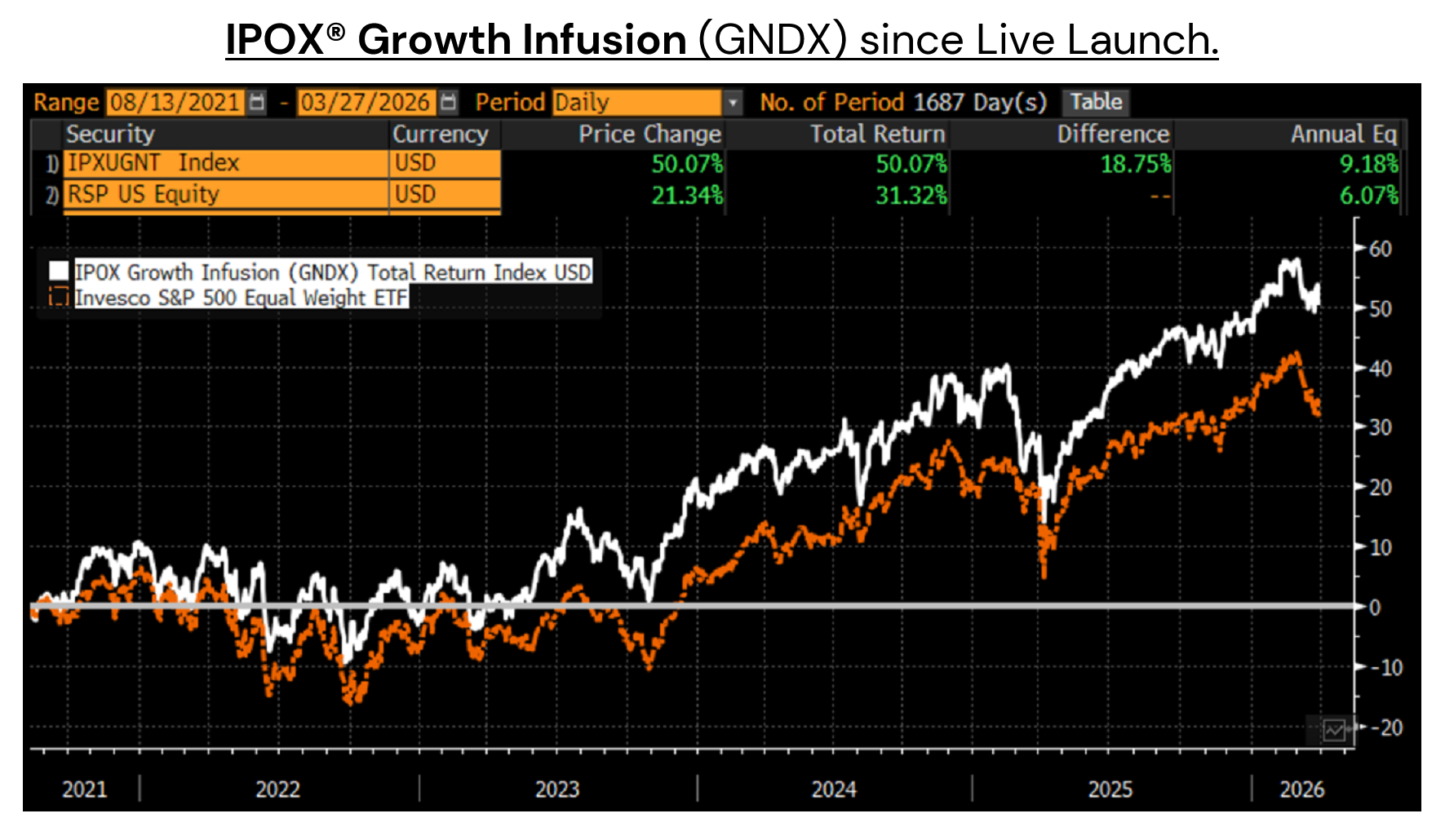

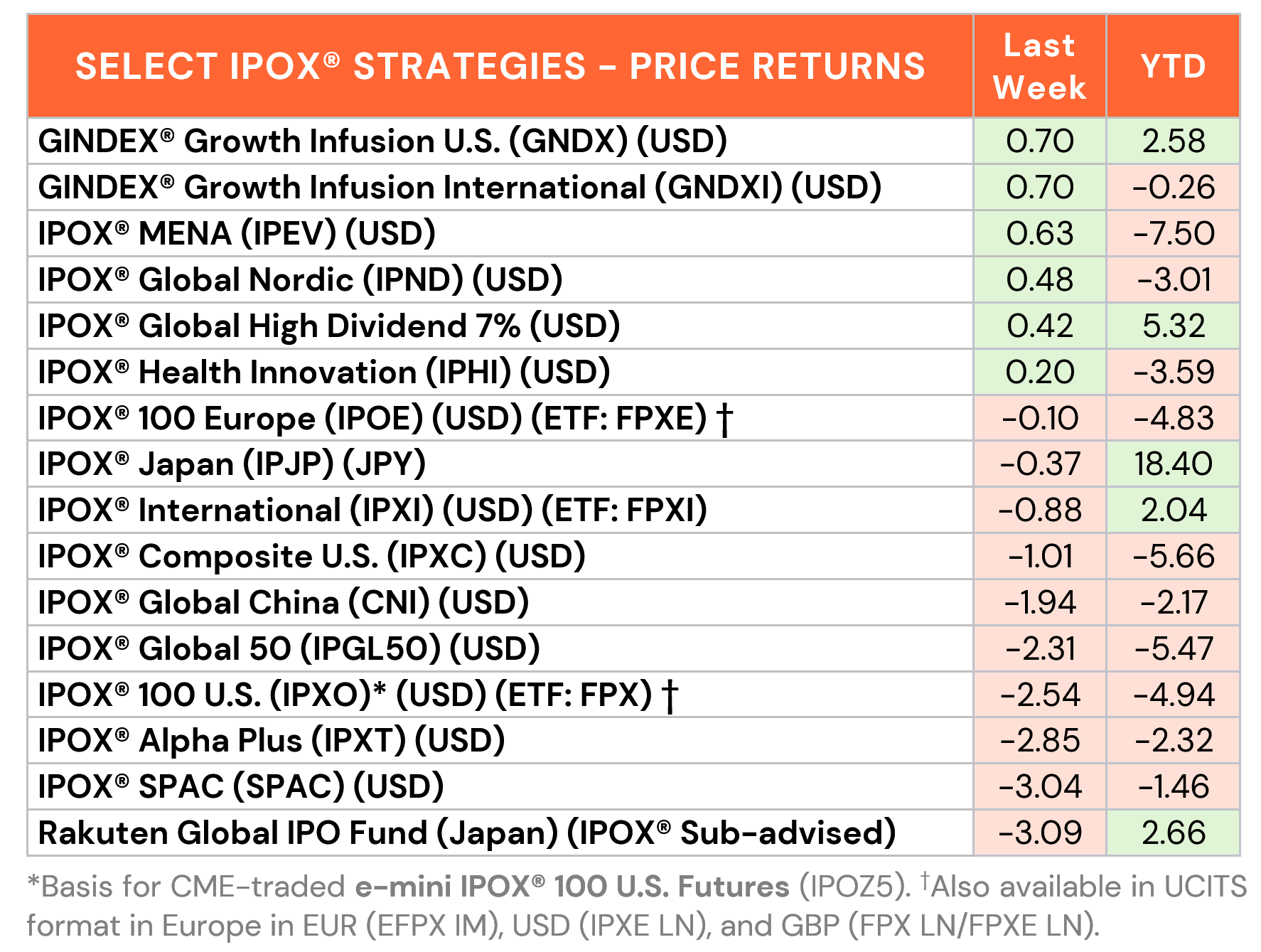

Performance Highlight: IPOX® High Dividend 7% gains to +5.32 YTD.

Movers: PayPay (PAYP), SKB (6990 HK), Fertiglobe (FERTIGLB DH).

CEO Schuster in the News: IPO window “wide open” for defense & energy firms.

INTERNATIONAL: With the exception of the IPOX® Global Nordic (IPDN), IPOX® Indexes focused on non-US stocks continued to weaken last week with the IPOX® Global China (CNI) and IPOX® Japan (IPJP) leading the way to fall to -2.17% and +18.40% YTD, respectively. A big finish to the week propelled key IPOX® Holding SKB Biopharma (6990 HK: +9.58%), while Softbank-linked firms semiconductor maker ARM (ARM US: +8.90%) and recently listed Fintech PayPay (PAYP US: +15.78%) also rose strongly. Amid surging crude oil prices and the start of the U.S. farming season, fertilizer makers Fertiglobe (FERTIGLB DH: +6.38%) and Canada’s Nutrien (NTR US: +1.23%) remained in focus.

THE IPOX® SPAC INDEX: The Index declined -3.04% last week, turning to -1.46% YTD. Both the best and worst performers came from the oil and gas space, with Permian Resources (PR US: +7.87%) reaching a new all-time high, while newly listed deSPAC oil and gas operator Presidio Production (FTW US: -15.02%) was the weakest performer amid continued volatility. No SPAC announced merger targets. Three SPACs completed combinations, including Crane Harbor Acquisition (CHAC US) with Canadian quantum data center start-up Xanadu (XNDU US). Three new SPAC IPOs were launched in the U.S.

ECM REVIEW: Global markets saw 24 firms go public last week, raising a total of $2.46 billion and posting an average gain of +24.16% (Median: +11.00%). Hong Kong saw strong activity led by networking solutions provider FS COM (3355 HK), which gained +10.58% on a $213 million raise. Other notable debuts included logistics robotics firm Galaxis Technology (2729 HK), which surged +92.08% ($78 million), automotive display maker New Vision Automotive (2632 HK: +31.22%, $92 million), and battery materials firm Nsing Technologies (2701 HK: +19.17%, $131 million). In Europe, Norwegian underwater tech firm General Oceans (GENO NO) rose +20.95% ($109 million). Australian gold miner Valiant Gold (VAL AU: +20.00%, $53 million) and Japanese business succession specialist Seiwa Holdings (523A JP: +21.60%, $44 million) also performed well.

This week, U.S. deal flow features oil and gas drilling equipment firm HMH Holding (HMH US), targeting up to $231 million. Discussing the offering in Reuters, IPOX® CEO Josef Schuster noted that the current price-sensitive buyer's market is exceptionally receptive for energy listings. In separate coverage regarding defense contractor AEVEX's IPO filing, Schuster added that the listing window for defense stocks is also "wide open" due to generational growth in military spending.

Hong Kong expects the wave of listings to continue, led by silicon wafer maker EpiWorld (2726 HK, $209 million) and robotics firm Huayan Robotics (1021 HK, $175 million). They are joined by traditional medicine provider Tong Ren Tang Healthcare (2667 HK, $115 million), medical software firm Diagens (2526 HK, $101m), audio chip designer FourSemi (3625 HK, $77m), AI computer vision firm Extreme Vision (6636 HK, $64m) and copper arts & crafts firm Tongshifu (664 HK, $64m).

INTERNATIONAL: Respective IPOX® Indexes focused on non-U.S. stocks fell last week, pressured by asset allocation selling in the benchmarks with big declines across mining stocks, e.g... While the IPOX® MENA (IPEV) remained the worst performing IPOX® Strategy YTD, the unlevered and actively managed IPOX® Global High Dividend 7% Strategy surged to a large +300 bps. vs. its benchmark YTD, while also doubling the benchmarks dividend yield. Stocks with most upside focus here continued to be China’s battery maker Amperex (3750 HK: +12.40%) and Norway’s oil producer Var Energy (VAR NO: +16.42%), while a big upgrade from HSBC propelled British semiconductor maker U.S.-traded ARM (ARM US: +14.34%).

THE IPOX® SPAC INDEX: The Index edged up 0.18% on the week, bringing year-to-date performance to 1.63%. Satellite earth imagining company Planet Labs (PL US: +36.47%) was the best performer amid strong earnings and guidance, while autonomous trucking company Kodiak AI (KDK US: -11.70%) declined despite outlining plans to accelerate autonomous driving deployment. Two SPACs announced merger targets, including New Providence Acquisition III (NPAC US), which agreed to combine with digital asset wealth platform Abra Financial. Two SPACs completed business combinations, including Bleichroeder Acquisition (BACQ US) with autonomous aviation company Merlin Labs (MRLN US). Corporate activity also continued in the deSPAC space, with OTC-traded 12/2023 deSPAC ECD Automotive Design was taken private by ATW Classic Equity. Two new SPAC IPOs were launched in the U.S.

ECM DEALS & OUTLOOK: 14 global IPOs raised $3.06 billion last week with an average gain of +117.85% (Median: +25.52%). In the U.S., senior housing REIT Janus Living (JAN US: +18.00%) gained on an $840 million raise. Deal flow in accessible markets was robust, featuring the $395 million debut of German tank components maker Vincorion (V1NC GR: +12.06%) and the $436 million IPO of Norwegian oil tanker operator Capital Tankers (CAPT NO -6.79%). In Asia, Chinese circuit board maker Delton Technology (1989 HK: +33.56%, $422m surged, while South Korean immunology biopharma IMBiologics (493280 KS: +300.00%, $35m) skyrocketed. Other notable listings included Malaysian private healthcare provider Sunway Healthcare (SUNMED MK: +31.03%, $679 million) and Swedish-listed German industrial acquirer ARENIT Industrie (ARENISDB SS: -3.25%, $63 million).

This week, global IPOs are led by Hong Kong listings of data center equipment provider FS.COM (3355 HK, $213m), semiconductor designer Nsing Technologies (2701 HK, $131m), automotive heads-up display manufacturer New Vision Automotive (2632 HK, $99m), and logistics robotics firm Galaxis Technology Group (2729 HK, $96m). In Europe, Norwegian underwater tech holding company General Oceans (GENO NO) aims for $109 million on the Euronext Oslo. Meanwhile, in Japan, manufacturing company succession specialist Seiwa Holdings (523A JP) plans a $44 million debut.