SchusterWatch #834 (3/23/2026)

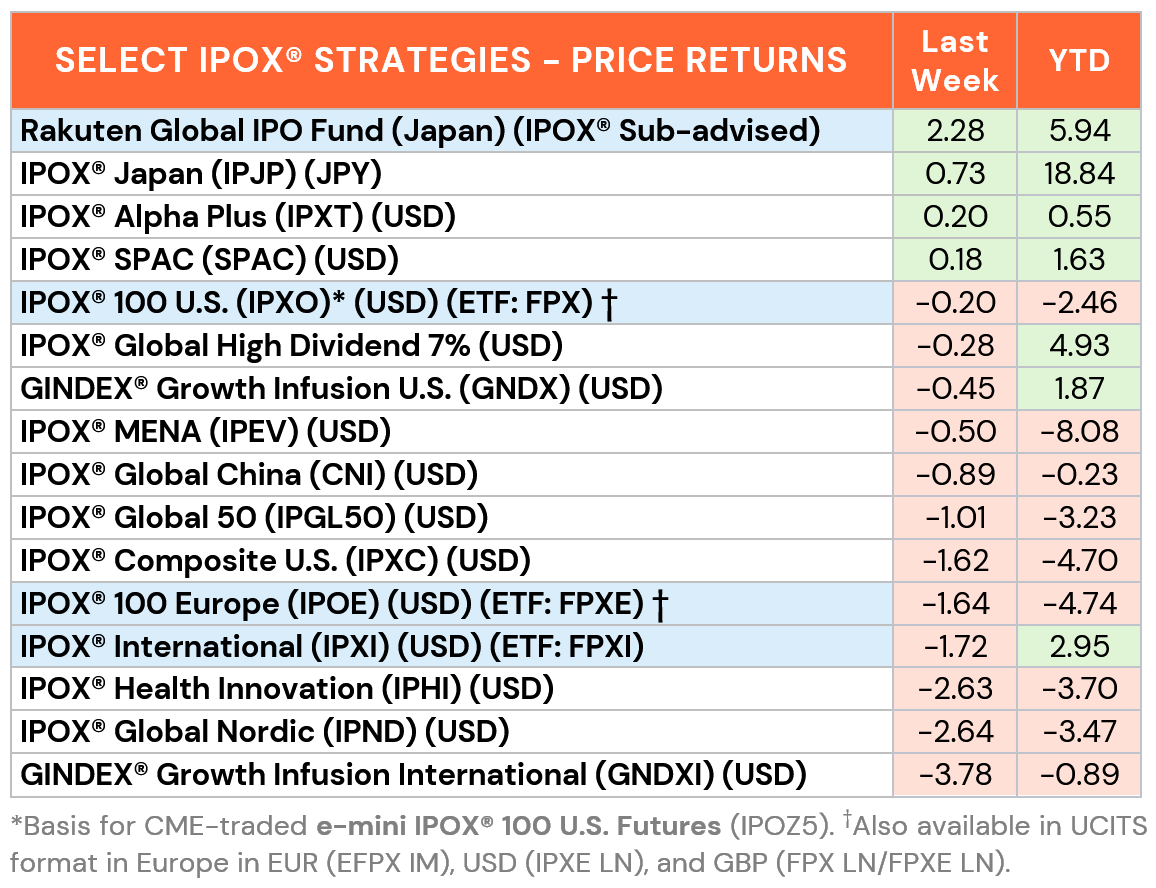

-0.20% Weekly Decline: IPOX® 100 US (FPX) remains strong vs. benchmarks.

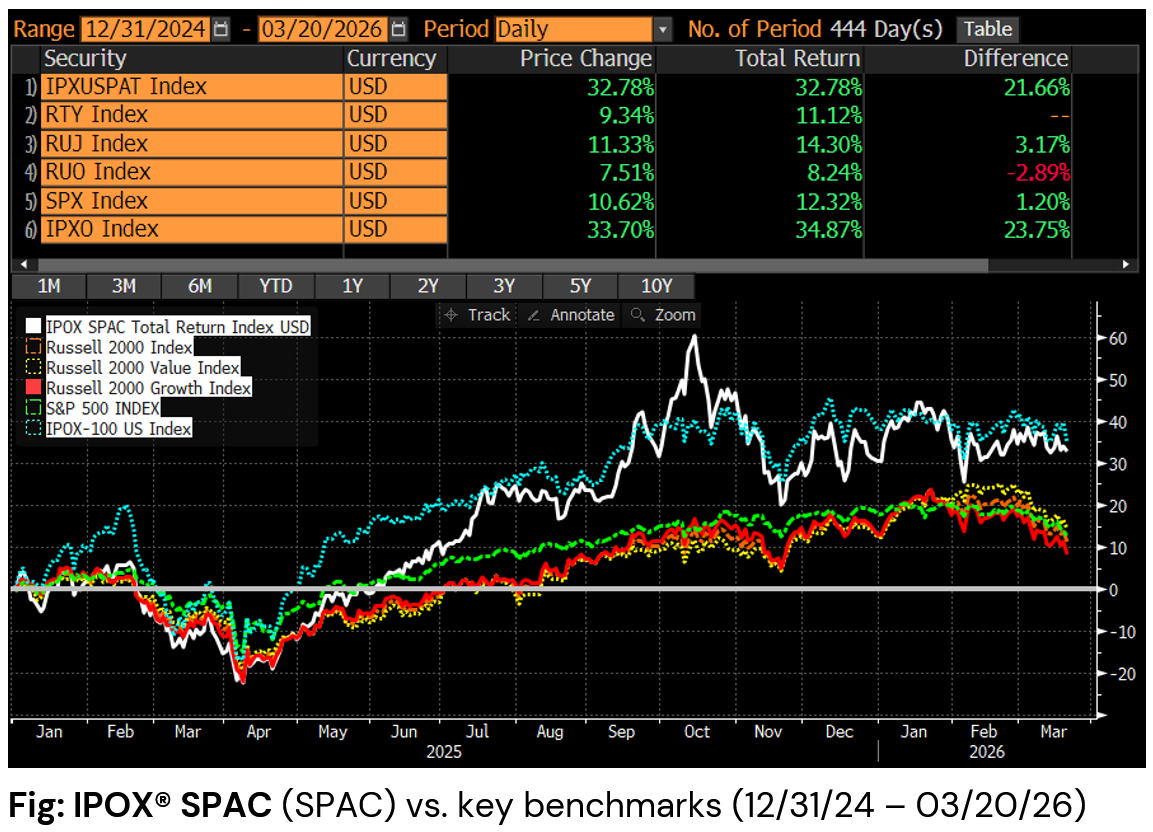

Safe Haven: IPOX® SPAC gains during volatile week in global equities.

Movers: Amperex (3750 HK), Brightspring (BTSG), Var Energy (VAR NO).

Global Deal Flow: IPOs raise $3B, defense play Vincorion climbs 12% on debut.

OVERVIEW: Most IPOX® Indexes outperformed significantly during Futures & Options expiration and Fed week as uncertainty over the length of the war in the Middle East drove another round of selling in the broad and derivatives-heavy global benchmarks, while inflation fears drove interest rates higher, equity risk declined (VIX: -1.51%), crude oil remained well-bid and metals and copper plunged.

UNITED STATES: The IPOX® 100 U.S., key post-IPO performance benchmark and underlying for the $1.5bn “FPX” ETF – shed just -0.20% to -2.46% YTD, +178 bps., +170 bps. and +148 bps. ahead of the Nasdaq 100 (NDX), S&P 500 (SPX) and Russell 2000 (RTY), benchmarks for U.S. stocks. 32% of portfolio holdings rose with the average (median) equally weighted firm declining by -1.14% (-1.47%), lagging the applied market-cap weighted IPOX® 100 US Index. Application software maker DigitalOcean (DOCN US: +20.43%), online insurance service provider Lemonade (LMND US: +16.37%) and health care services provider BrightSpring (BTSG US: +7.57%) recorded notable gains on post-earnings Momentum and IPO M&A speculation, while software maker SailPoint (SAIL US: -20.71%) and communications equipment maker Credo (CRDO US: -12.14%) declined, following disappointing quarterly results.

OUTSTANDING: We note another strong week for the IPOX® SPAC (SPAC) as it de-coupled anew from U.S small-caps with the Russell 2000 (RTY) closing out last week in correction territory:

INTERNATIONAL: Respective IPOX® Indexes focused on non-U.S. stocks fell last week, pressured by asset allocation selling in the benchmarks with big declines across mining stocks, e.g... While the IPOX® MENA (IPEV) remained the worst performing IPOX® Strategy YTD, the unlevered and actively managed IPOX® Global High Dividend 7% Strategy surged to a large +300 bps. vs. its benchmark YTD, while also doubling the benchmarks dividend yield. Stocks with most upside focus here continued to be China’s battery maker Amperex (3750 HK: +12.40%) and Norway’s oil producer Var Energy (VAR NO: +16.42%), while a big upgrade from HSBC propelled British semiconductor maker U.S.-traded ARM (ARM US: +14.34%).

THE IPOX® SPAC INDEX: The Index edged up 0.18% on the week, bringing year-to-date performance to 1.63%. Satellite earth imagining company Planet Labs (PL US: +36.47%) was the best performer amid strong earnings and guidance, while autonomous trucking company Kodiak AI (KDK US: -11.70%) declined despite outlining plans to accelerate autonomous driving deployment. Two SPACs announced merger targets, including New Providence Acquisition III (NPAC US), which agreed to combine with digital asset wealth platform Abra Financial. Two SPACs completed business combinations, including Bleichroeder Acquisition (BACQ US) with autonomous aviation company Merlin Labs (MRLN US). Corporate activity also continued in the deSPAC space, with OTC-traded 12/2023 deSPAC ECD Automotive Design was taken private by ATW Classic Equity. Two new SPAC IPOs were launched in the U.S.

ECM DEALS & OUTLOOK: 14 global IPOs raised $3.06 billion last week with an average gain of +117.85% (Median: +25.52%). In the U.S., senior housing REIT Janus Living (JAN US: +18.00%) gained on an $840 million raise. Deal flow in accessible markets was robust, featuring the $395 million debut of German tank components maker Vincorion (V1NC GR: +12.06%) and the $436 million IPO of Norwegian oil tanker operator Capital Tankers (CAPT NO -6.79%). In Asia, Chinese circuit board maker Delton Technology (1989 HK: +33.56%, $422m surged, while South Korean immunology biopharma IMBiologics (493280 KS: +300.00%, $35m) skyrocketed. Other notable listings included Malaysian private healthcare provider Sunway Healthcare (SUNMED MK: +31.03%, $679 million) and Swedish-listed German industrial acquirer ARENIT Industrie (ARENISDB SS: -3.25%, $63 million).

This week, global IPOs are led by Hong Kong listings of data center equipment provider FS.COM (3355 HK, $213m), semiconductor designer Nsing Technologies (2701 HK, $131m), automotive heads-up display manufacturer New Vision Automotive (2632 HK, $99m), and logistics robotics firm Galaxis Technology Group (2729 HK, $96m). In Europe, Norwegian underwater tech holding company General Oceans (GENO NO) aims for $109 million on the Euronext Oslo. Meanwhile, in Japan, manufacturing company succession specialist Seiwa Holdings (523A JP) plans a $44 million debut.