SchusterWatch #832 (3/9/2026)

IPOX® Indexes Momentum tempered by war, rising U.S. bond yields.

Hanging in there: IPOX® 100 US (ETF: FPX) falls -2.42% to -0.67% YTD.

Pre-IPO investors knocked as Robinhood vehicle plunges -16% on debut.

US IPO Outlook: Softbank-backed PayPay set to raise $1 billion this week.

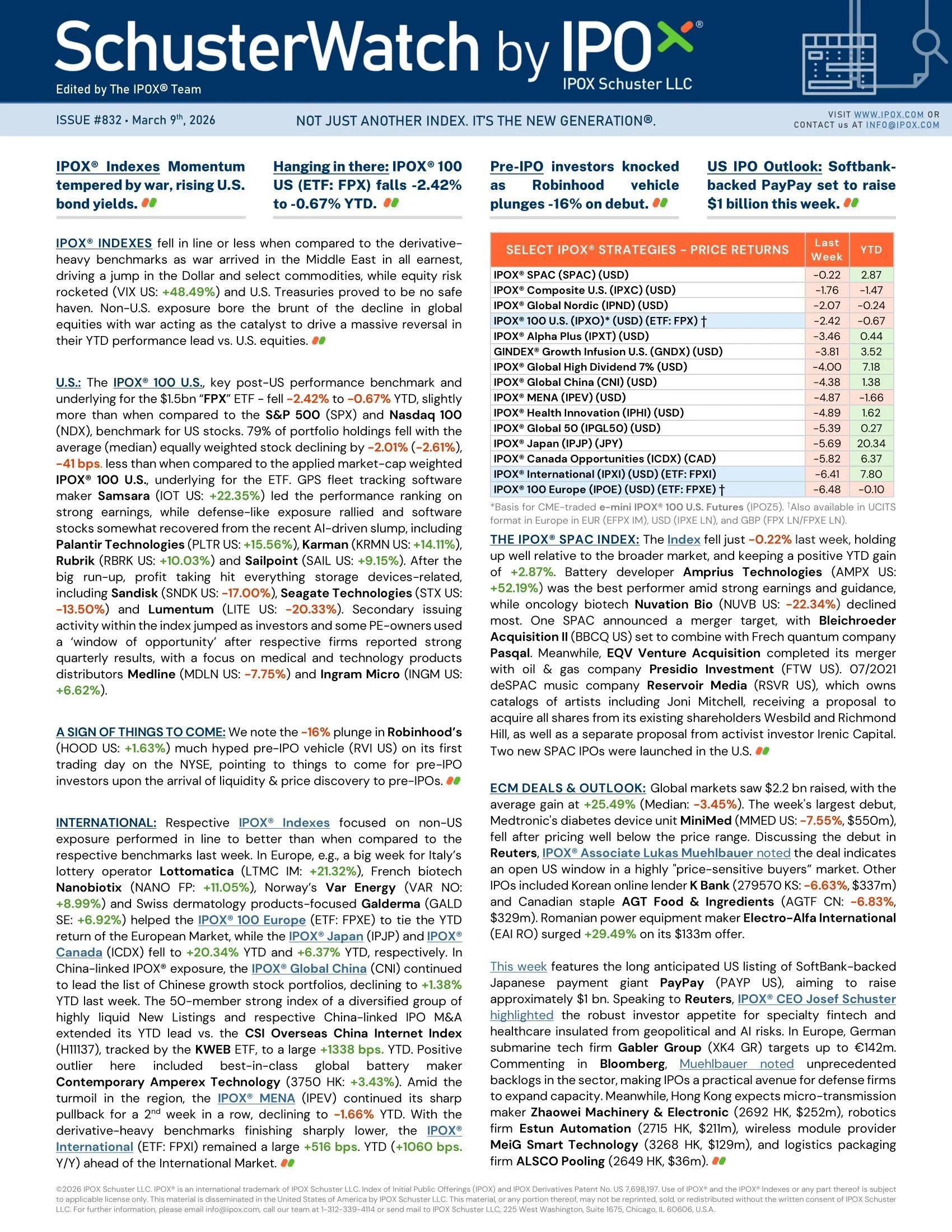

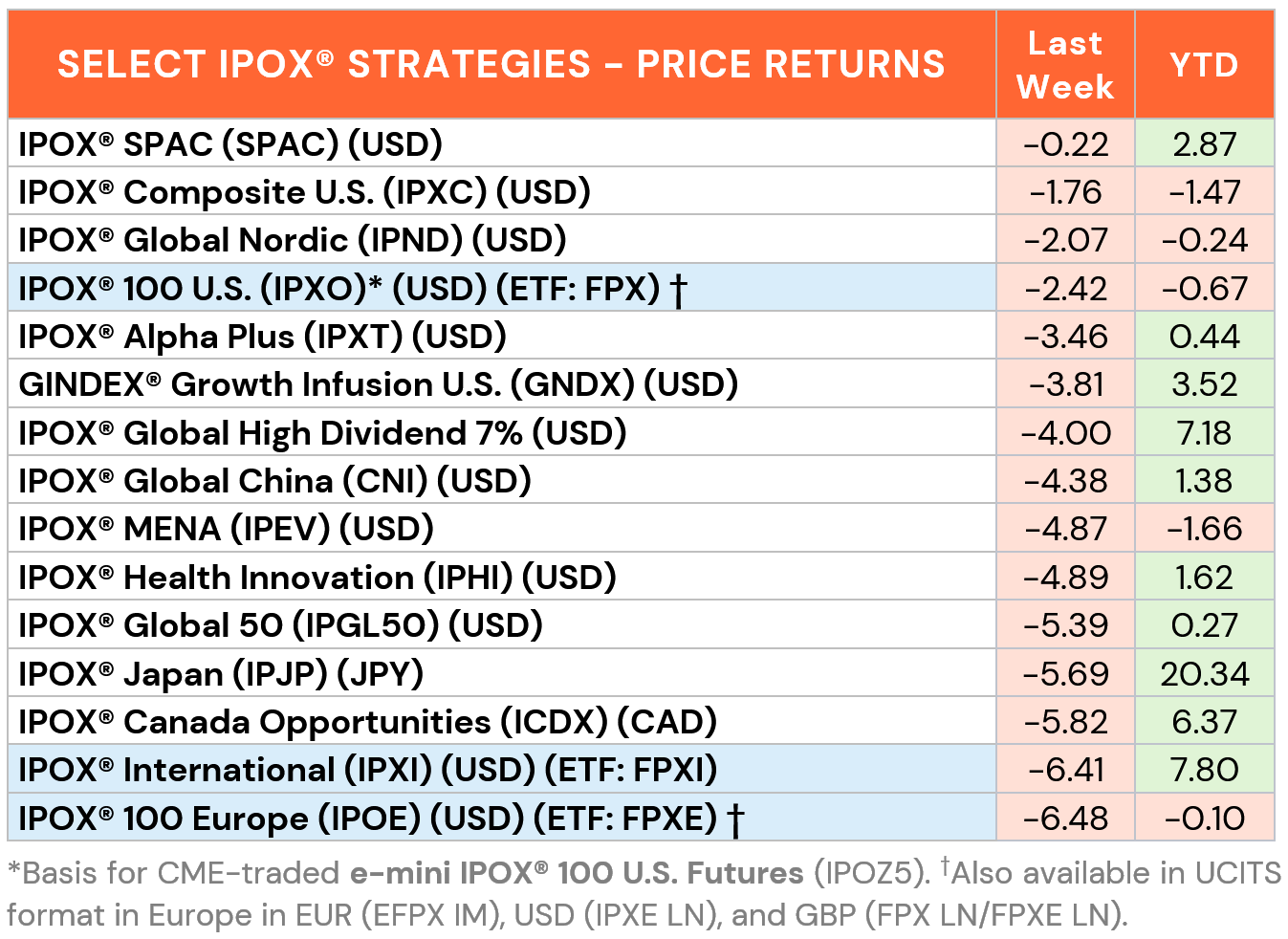

IPOX® INDEXES fell in line or less when compared to the derivative-heavy benchmarks as war arrived in the Middle East in all earnest, driving a jump in the Dollar and select commodities, while equity risk rocketed (VIX US: +48.49%) and U.S. Treasuries proved to be no safe haven. Non-U.S. exposure bore the brunt of the decline in global equities with war acting as the catalyst to drive a massive reversal in their YTD performance lead vs. U.S. equities.

U.S.: The IPOX® 100 U.S., key post-US performance benchmark and underlying for the $1.5bn “FPX” ETF - fell -2.42% to -0.67% YTD, slightly more than when compared to the S&P 500 (SPX) and Nasdaq 100 (NDX), benchmark for US stocks. 79% of portfolio holdings fell with the average (median) equally weighted stock declining by -2.01% (-2.61%), -41 bps. less than when compared to the applied market-cap weighted IPOX® 100 U.S., underlying for the ETF. GPS fleet tracking software maker Samsara (IOT US: +22.35%) led the performance ranking on strong earnings, while defense-like exposure rallied and software stocks somewhat recovered from the recent AI-driven slump, including Palantir Technologies (PLTR US: +15.56%), Karman (KRMN US: +14.11%), Rubrik (RBRK US: +10.03%) and Sailpoint (SAIL US: +9.15%). After the big run-up, profit taking hit everything storage devices-related, including Sandisk (SNDK US: -17.00%), Seagate Technologies (STX US: -13.50%) and Lumentum (LITE US: -20.33%). Secondary issuing activity within the index jumped as investors and some PE-owners used a ‘window of opportunity’ after respective firms reported strong quarterly results, with a focus on medical and technology products distributors Medline (MDLN US: -7.75%) and Ingram Micro (INGM US: +6.62%).

A SIGN OF THINGS TO COME: We note the -16% plunge in Robinhood’s (HOOD US: +1.63%) much hyped pre-IPO vehicle (RVI US) on its first trading day on the NYSE, pointing to things to come for pre-IPO investors upon the arrival of liquidity & price discovery to pre-IPOs.

INTERNATIONAL: Respective IPOX® Indexes focused on non-US exposure performed in line to better than when compared to the respective benchmarks last week. In Europe, e.g., a big week for Italy’s lottery operator Lottomatica (LTMC IM: +21.32%), French biotech Nanobiotix (NANO FP: +11.05%), Norway’s Var Energy (VAR NO: +8.99%) and Swiss dermatology products-focused Galderma (GALD SE: +6.92%) helped the IPOX® 100 Europe (ETF: FPXE) to tie the YTD return of the European Market, while the IPOX® Japan (IPJP) and IPOX® Canada (ICDX) fell to +20.34% YTD and +6.37% YTD, respectively. In China-linked IPOX® exposure, the IPOX® Global China (CNI) continued to lead the list of Chinese growth stock portfolios, declining to +1.38% YTD last week. The 50-member strong index of a diversified group of highly liquid New Listings and respective China-linked IPO M&A extended its YTD lead vs. the CSI Overseas China Internet Index (H11137), tracked by the KWEB ETF, to a large +1338 bps. YTD. Positive outlier here included best-in-class global battery maker Contemporary Amperex Technology (3750 HK: +3.43%). Amid the turmoil in the region, the IPOX® MENA (IPEV) continued its sharp pullback for a 2nd week in a row, declining to -1.66% YTD. With the derivative-heavy benchmarks finishing sharply lower, the IPOX® International (ETF: FPXI) remained a large +516 bps. YTD (+1060 bps. Y/Y) ahead of the International Market.

THE IPOX® SPAC INDEX: The Index fell just -0.22% last week, holding up well relative to the broader market, and keeping a positive YTD gain of +2.87%. Battery developer Amprius Technologies (AMPX US: +52.19%) was the best performer amid strong earnings and guidance, while oncology biotech Nuvation Bio (NUVB US: -22.34%) declined most. One SPAC announced a merger target, with Bleichroeder Acquisition II (BBCQ US) set to combine with Frech quantum company Pasqal. Meanwhile, EQV Venture Acquisition completed its merger with oil & gas company Presidio Investment (FTW US). 07/2021 deSPAC music company Reservoir Media (RSVR US), which owns catalogs of artists including Joni Mitchell, receiving a proposal to acquire all shares from its existing shareholders Wesbild and Richmond Hill, as well as a separate proposal from activist investor Irenic Capital. Two new SPAC IPOs were launched in the U.S.

ECM DEALS & OUTLOOK: Global markets saw $2.2 bn raised, with the average gain at +25.49% (Median: -3.45%). The week's largest debut, Medtronic's diabetes device unit MiniMed (MMED US: -7.55%, $550m), fell after pricing well below the price range. Discussing the debut in Reuters, IPOX® Associate Lukas Muehlbauer noted the deal indicates an open US window in a highly "price-sensitive buyers” market. Other IPOs included Korean online lender K Bank (279570 KS: -6.63%, $337m) and Canadian staple AGT Food & Ingredients (AGTF CN: -6.83%, $329m). Romanian power equipment maker Electro-Alfa International (EAI RO) surged +29.49% on its $133m offer.

This week features the long anticipated US listing of SoftBank-backed Japanese payment giant PayPay (PAYP US), aiming to raise approximately $1 bn. Speaking to Reuters, IPOX® CEO Josef Schuster highlighted the robust investor appetite for specialty fintech and healthcare insulated from geopolitical and AI risks. In Europe, German submarine tech firm Gabler Group (XK4 GR) targets up to €142m. Commenting in Bloomberg, Muehlbauer noted unprecedented backlogs in the sector, making IPOs a practical avenue for defense firms to expand capacity. Meanwhile, Hong Kong expects micro-transmission maker Zhaowei Machinery & Electronic (2692 HK, $252m), robotics firm Estun Automation (2715 HK, $211m), wireless module provider MeiG Smart Technology (3268 HK, $129m), and logistics packaging firm ALSCO Pooling (2649 HK, $36m).