SchusterWatch #829 (2/16/2026)

Japan propels IPOX® International (FPXI) to big week; GINDEX® Record.

IPOX® 100 U.S. (FPX) outpaces benchmarks as AI fears crush Multiples.

Movers: SOLS US, Q US, VSAT US, 316140 KS, 285A JP, MICC NA, CSG NA.

Only 2 IPOs seen amid U.S. Presidents Day Holiday and Chinese New Year.

MOST IPOX® STRATEGIES GAIN STRONGLY: Ahead of February Options expiration and the shortened U.S. trading week, most IPOX® Indexes strongly outpaced their benchmarks amid 1) the tug of war between strong earnings and the fears over the disruptive impact of AI crushing respective Multiples and driving higher equity risk (VIX: +15.99%), 2) huge gains amongst select IPOX® Portfolio holdings and 3) declining rates on strong U.S. government debt auction results and muted inflation numbers.

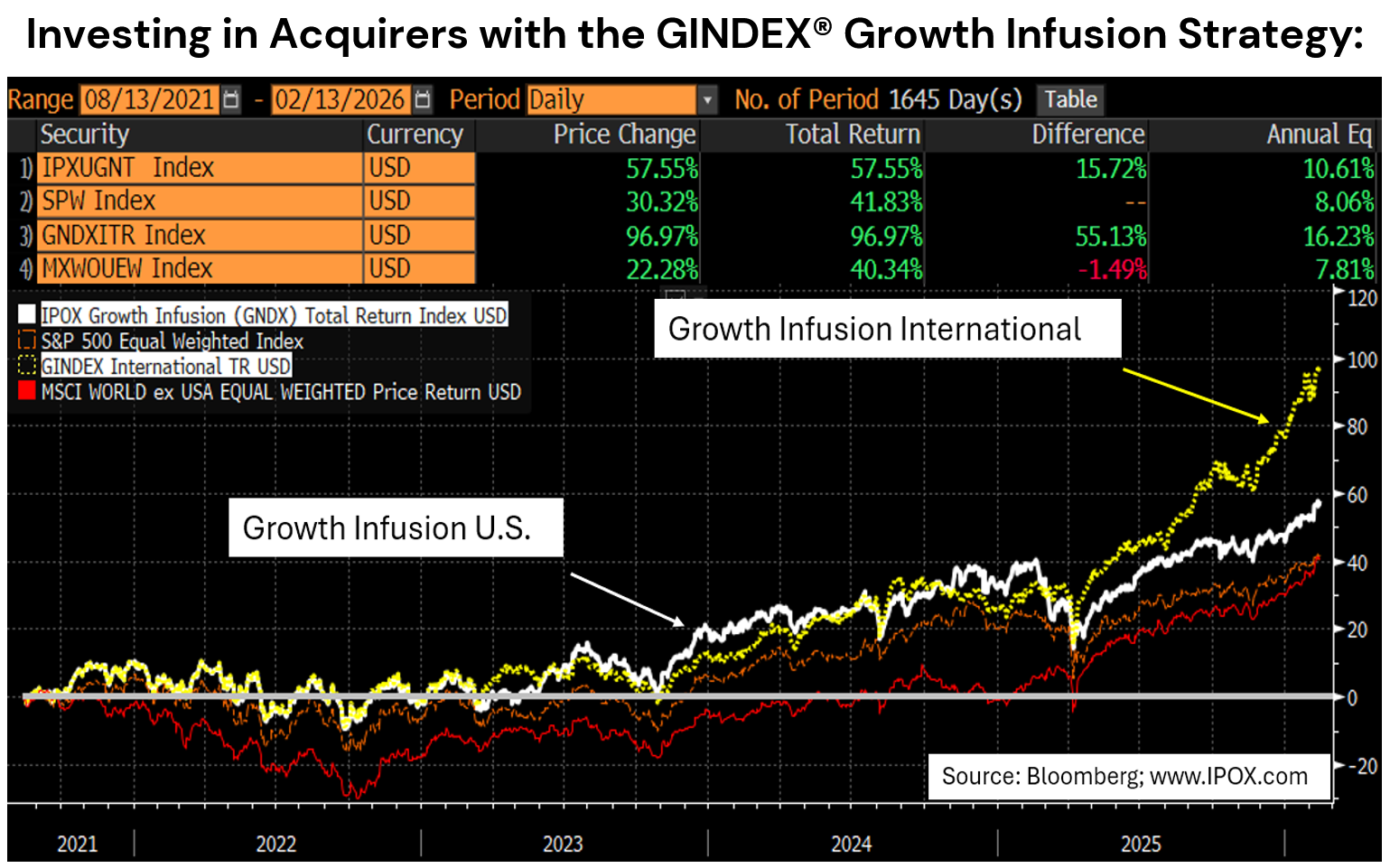

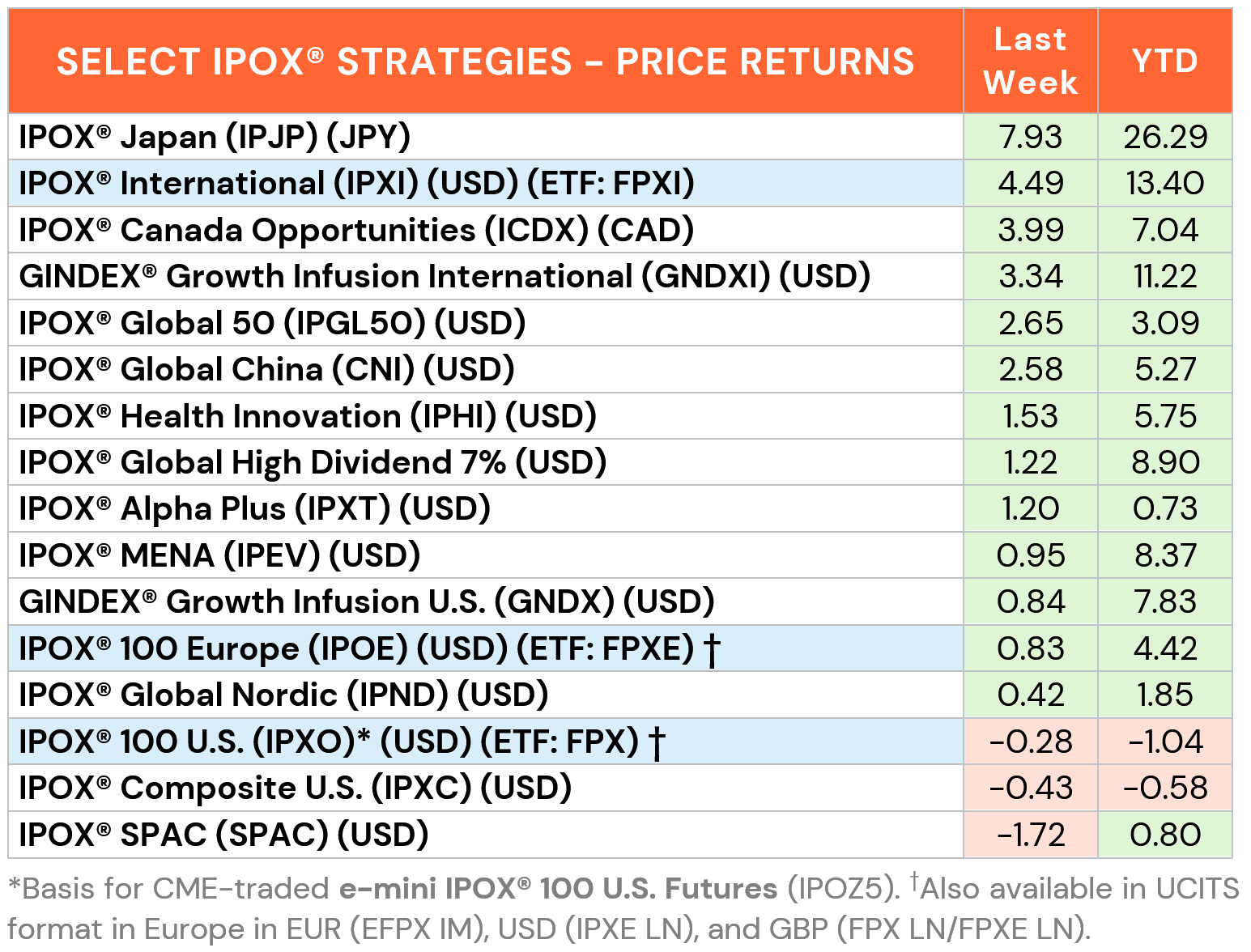

INTERNATIONAL: The IPOX® Japan (IPJP), IPOX® Canada Opportunities (ICDX) and IPOX® Global China (CNI) drove most gains in the IPOX® International (ETF: FPXI) with the portfolio adding +4.49% to +13.40% YTD, almost doubling the YTD gain in benchmark MSCI World ex USA (MXWOU). Best in class-sector exposure drove the good showing, including Korean Financial IPO M&A Woori Financial (316140 KS: +20.03%), Japanese memory chipmaker IPO Kioxia (285A JP: +19.64%), Japanese financials IPO Rakuten Bank (5838 JP: +10.24%), Canadian online retailer IPO Groupe Dynamite (GRDG CT: +8.51% and South African mining Spin-off Valterra Platinum (VALT LN: +8.15%). Weak earnings pressured highly shorted recent Netherlands-based IPO Magnum Ice Cream (MICC NA: -14.05%), while fears over corruption/kick-back schemes pressured European defense play IPO CSG (CSG NA: -8.74%).

UNITED STATES: Big swings characterized trading in the IPOX® 100 U.S. (ETF: FPX) with good earnings unable to fully compensate for rotation- and AI-driven declines in some of the IPOX® heavyweights, which continue to be affected from an unabated contraction in multiples hitting the broader technology sector. Significant gains in recent spin-offs and specialty IPOs, such as specialty chemicals makers Solstice (SOLS US: +20.73%) and Qnity Electronics (Q US: +13.71%), EV maker IPO Rivian (RIVN US: +19.80%), wireless network operator IPO ViaSat (VSAT US: +17.15%) and hospital group IPO M&A Tenet Healthcare (THC US: +14.76%) was still enough to propel the IPOX® 100 U.S. (FPX) beyond the benchmarks last week and retain last year big gains.

GINDEX® OUTPERFORMANCE: We note the fresh weekly all-time High in our GINDEX® Growth Infusion Strategies which focus on providing bespoke J-curve exposure to acquiring firms targeting predominantly IPOs Internationally (GNDXI) and in the United States (GNDX):

THE IPOX® SPAC INDEX: The Index declined -1.72% last week, but remains up 0.80% year-to-date. Data center infrastructure supplier Vertiv (VRT US: +19.92%) was the best performer after reporting better-than-expected revenue and raising guidance amid continued demand tied to AI-driven data center buildouts. Clinical-stage biopharmaceutical company Disc Medicine (IRON US: -29.82%) plunged after a regulatory setback, as the FDA rejected the accelerated new drug application for its lead drug candidate, bitopertin, and extended the review timeline. No SPACs announced merger targets. Churchill Capital X (CCCX US) completed its merger with neutral-atom quantum computing company Infleqtion (INFQ US), which is expected to begin trading on the NYSE following the Presidents’ Day holiday on February 17. 10 new SPAC IPOs launched in the U.S. during the week.

ECM DEALS & OUTLOOK: Global markets saw 26 IPOs raise $4.3 billion last week, new listings delivered an average gain of +59.06% (Median: +23.27%). In accessible markets, Hong Kong saw heavy deal flow led by cloud computing chip designer Montage Technology (6809 HK), which surged +73.08% following its $1.04 billion offer. AI data firm Beijing Haizhi Technology (2706 HK: +242.20%, $97 million) and outdoors gear maker Ridge Outdoor International (2720 HK: +104.90%, $44 million) also saw outsized gains. Larger, more muted listings included EV battery tech firm Wuxi Lead Intelligent Equipment (470 HK: -0.87%, $631 million), AI SoC chipmaker Axera Semiconductor (600 HK: +0.21%, $379 million), and heat shrink cable maker Shenzhen Woer (9981 HK: +2.94%, $360 million).

In the U.S., solar power firm Solv Energy (MWH US) gained +29.36% on a $589 million raise. Brazilian fintech AGI Inc. (AGBK US) fell -8.33% on its downsized $240 million offer. Discussing the deal in Reuters, IPOX® Associate Muehlbauer noted potential overhang risks. Meanwhile, fuel distributor ARKO Petroleum (APC US: 0.00%, $200m) traded flat, with IPOX® VP Kat Liu noting investor caution.

Amid the shortened U.S. trading week, just 2 sizable IPOs are on the calendar this week, both listing in Japan. Japanese-Austrian biotechnology company Innovacell (504A JP) targets a $78 million raise, joined by IT and gaming-focused recruitment firm Geekly (505A JP) with a $39 million offering, which consists entirely of a secondary share sale.