SchusterWatch #828 (2/9/2026)

Market Swoon: IPOX® Strategies well supported after wild trading week.

IPOX®’s Winning Formula: Earnings drive IPOX® 100 U.S. (ETF: FPX) strength.

Movers: LITE, ALAB, VSCO, COCO, MDLN, RDDT, MICC NA, VOLCARB SS.

IPO Window Wide Open: More IPOs lined up during 2nd week of February.

IPOX® STRATEGIES WELL SUPPORTED: Last week’s trading was characterized by big swings across select asset classes driven by fears over the potential of AI to desolate certain economic sectors, which temporarily also propelled equity risk. With debt well-bid, this reverberated into massive swings in crypto and equity index spreads. Amid this backdrop - and a generally upbeat earnings picture for IPOX® - the IPOX® Strategies finished the week well supported, with key portfolios looking to extend last year’s market beating returns.

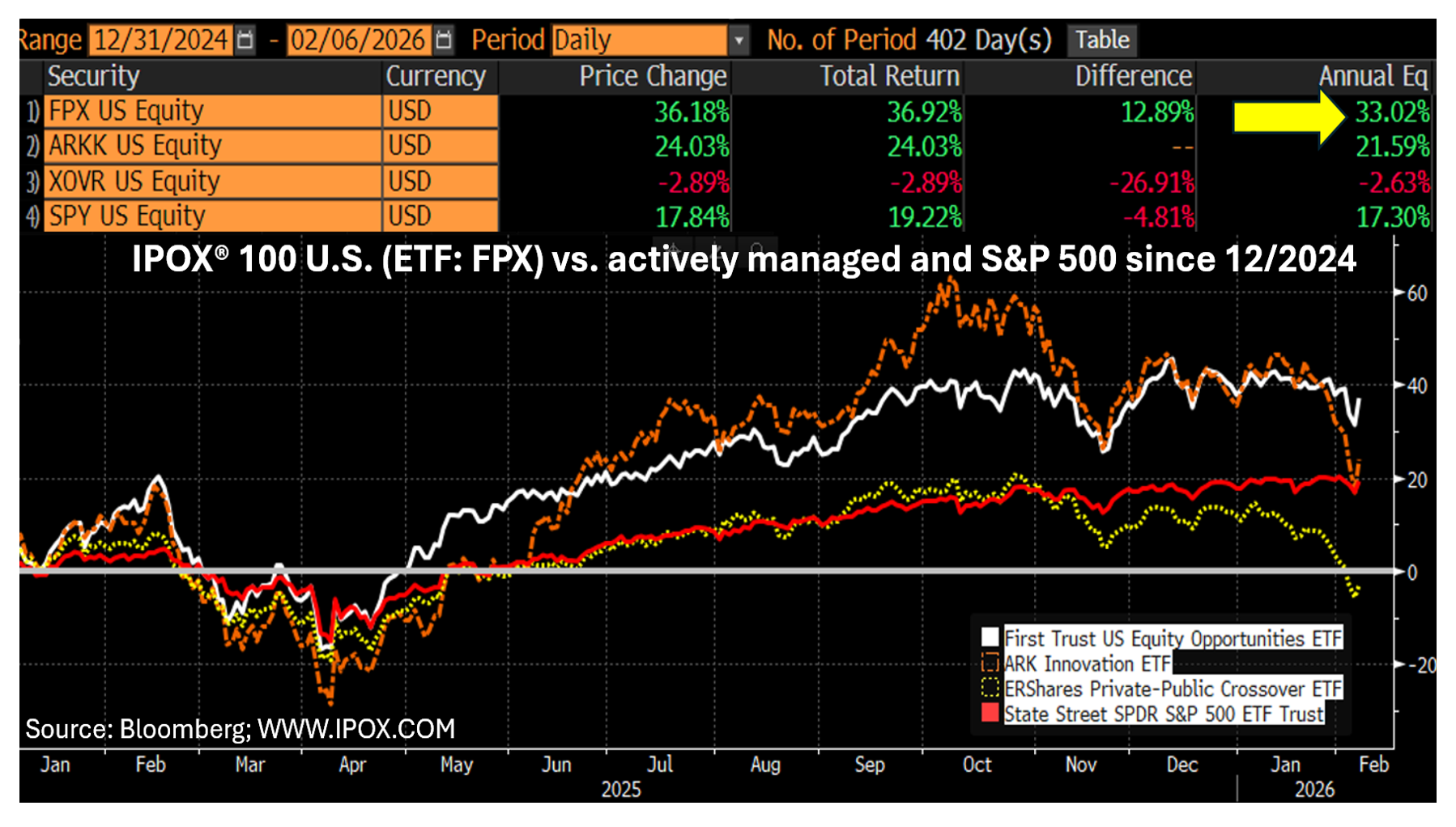

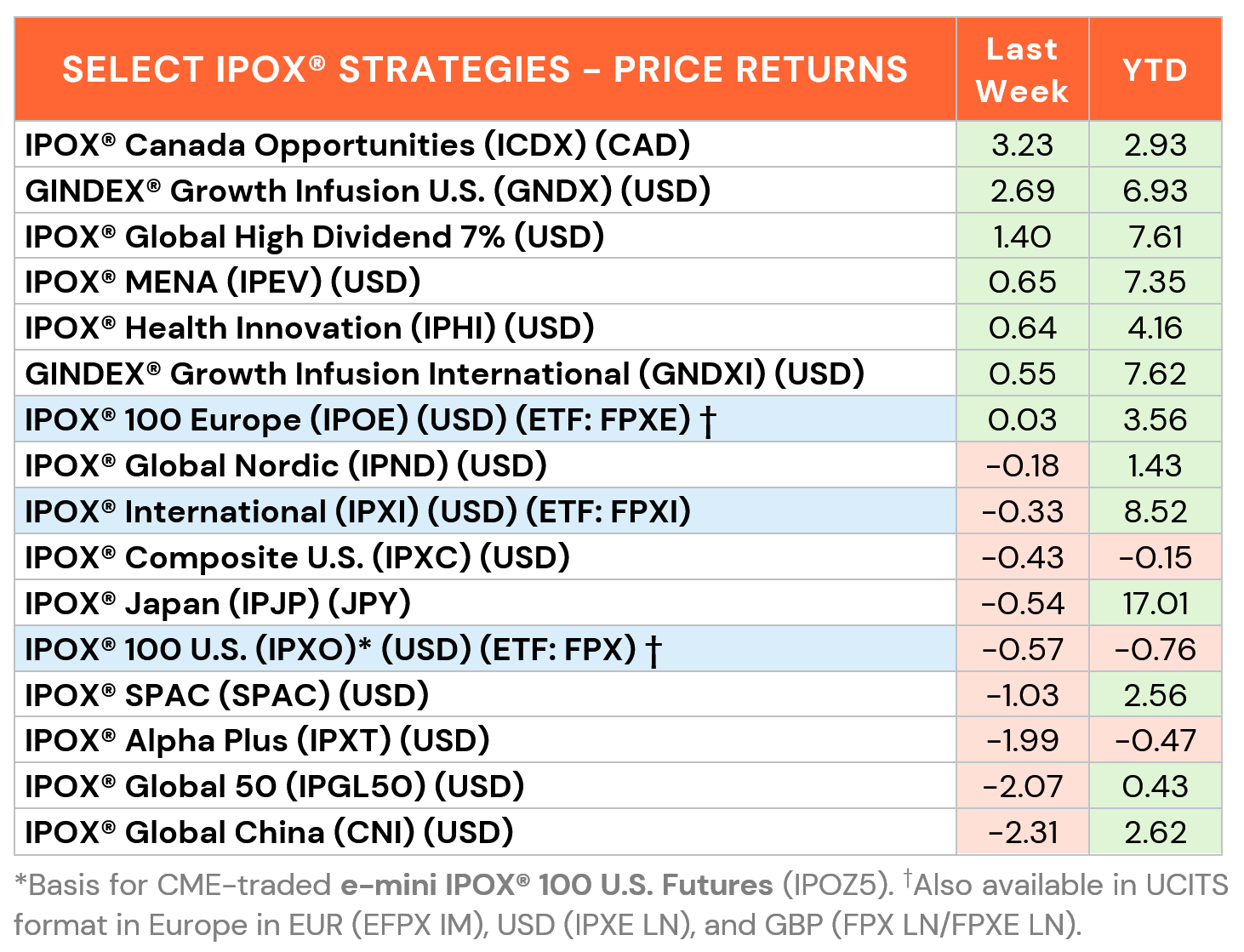

UNITED STATES: The IPOX® 100 U.S. (ETF: FPX) – key U.S. innovation gauge which invests in 100 U.S. New Listings between their IPO date and the time respective firms enter the S&P 500 (ETF: SPY) – fell by 0.57% to -0.76% YTD. With select IPOX® heavyweights under pressure, 59% of firms rose, with the average (median) equally weighted stock adding +0.01% (+1.55%), better than when compared to the IPOX® 100 U.S. (ETF: FPX). Earnings & post-earnings momentum drove strong gains in optical products maker Lumentum (LITE: +40.87%), connectivity solutions provider Astera Labs (ALAB US: +12.77%), apparels designer Victoria’s Secret (VSCO US: +14.55%) and beverage maker The Vita Coco Co. (COCO US: +10.52%), e.g. 12/2025 IPO IL-based medical products distributor P/E-backed Medline (MDLE US: +7.01%) now ranks as the 2nd most heavily weighted holding as other IPOX® heavyweights fell. Amid fears of how Google may affect user search, Reddit (RDDT US: -22.43%) sank despite strong earnings and a share buyback announcement. Strong earnings underpinned the jump in relative strength of the IPOX® 100 U.S. (ETF: FPX) vs. select actively managed ETFs during last week’s gyrations with pre-IPO exposure to SpaceX e.g. providing no panacea to shield respective ETFs from big declines:

MARKETS ABROAD continued to trade well supported with the IPOX® MENA (IPEV) leading the way anew, extending its YTD gain to +7.35%, while the IPOX® Japan (IPJP) managed to hang on to most of its YTD gain and the IPOX® 100 Europe (ETF: FPXE) rose marginally. With Miami-based hedge fund Citadel reducing its short position ahead of Sunday’s Superbowl, Spin-off Magnum Ice Cream (MICC NA: +8.63%) closed the week at yet another post-Spin off high, while select IPOX® Holdings joined the rally in global High Dividend stocks, such as Brazil’s Financial 06/2021 IPO Caixa Seguridade (CXSE3 BS: +5.26%). Sweden-based China-owned electric car maker Volvo Car (VOLCARB: -23.52%) slumped after U.S. Tariffs slashed Revenues.

THE IPOX® SPAC INDEX: The Index fell -1.03% last week, bringing YTD performance to 2.56%. Italian luxury fashion designer Ermenegildo Zegna (ZGN US: +19.56%) was the best performer after improving Q4 results. Quantum pure-play IonQ (IONQ US: -12.48%) was the worst, retreating amid volatility across quantum-related names. DT Cloud Star Acquisition (DTSQ US) announced a merger with stem cell therapy biotech PrimeGen US. No SPACs completed mergers, while 7 new SPACs launched in the U.S. Corporate activity continued among deSPACs, with the Exclusive Collective completing its acquisition of 02/2022 luxury travel and hospitality deSPAC Inspirato.

ECM DEALS & OUTLOOK: 23 companies raised a total of $6.8 billion, posting an average gain of +27.78% (Median: +14.82%). The week was headlined by the massive $1.5B debut of data center equipment maker Forgent Power (FPS US: +25.04%). IPOX® Associate Muehlbauer commented in Reuters, noting that the successful deal signaled healthy demand for infrastructure plays, driven by AI needs (read here).

Amid a big week for biotech IPOs, hair restoration firm VeraDermics (MANE US: +126.35%, $295m offer) was the week's top performer, while ophthalmology player SpyGlass Pharma (SGP US: +65.00%, $150m) also rallied. Conversely, larger clinical-stage listings struggled, including Eikon Therapeutics (EIKN US: -19.44%, $381m) and AgomAb Therapeutics (AGMB US: -8.44%, $200m). In Reuters coverage, IPOX® Associate Muehlbauer highlighted that the window for drugmakers remains open amid a "significant divergence in risk appetite" compared to other sectors (read here). In Hong Kong, billion-dollar listings saw steady debuts. Pork producer Muyuan Foods (2714 HK: +3.90%, $1.37 billion) and energy drink giant Eastroc Beverage (9980 HK: +8.23%, $1.30 billion) both traded up. Other notable deals included celebrity-backed Once Upon a Farm (OFRM US: +16.94%, $198m) and Bob's Discount Furniture (BOBS US: -3.12%, $331m).

The IPO calendar remains busy: Key U.S. deals include fintech Clear Street Group (CLRS US, $1.0 billion), Brazilian lender AGI (AGBK US, $720m) and solar infrastructure provider SOLV Energy (MWH US, $513m). In Hong Kong, chipmaker Montage (6809 HK) targets $902 million to fund its AI infrastructure expansion, joined by battery maker Wuxi Lead Intelligent Equipment (470 HK, $549m) and edge AI chipmaker Axera (600 HK, $379m).