SchusterWatch #818 (12/1/2025)

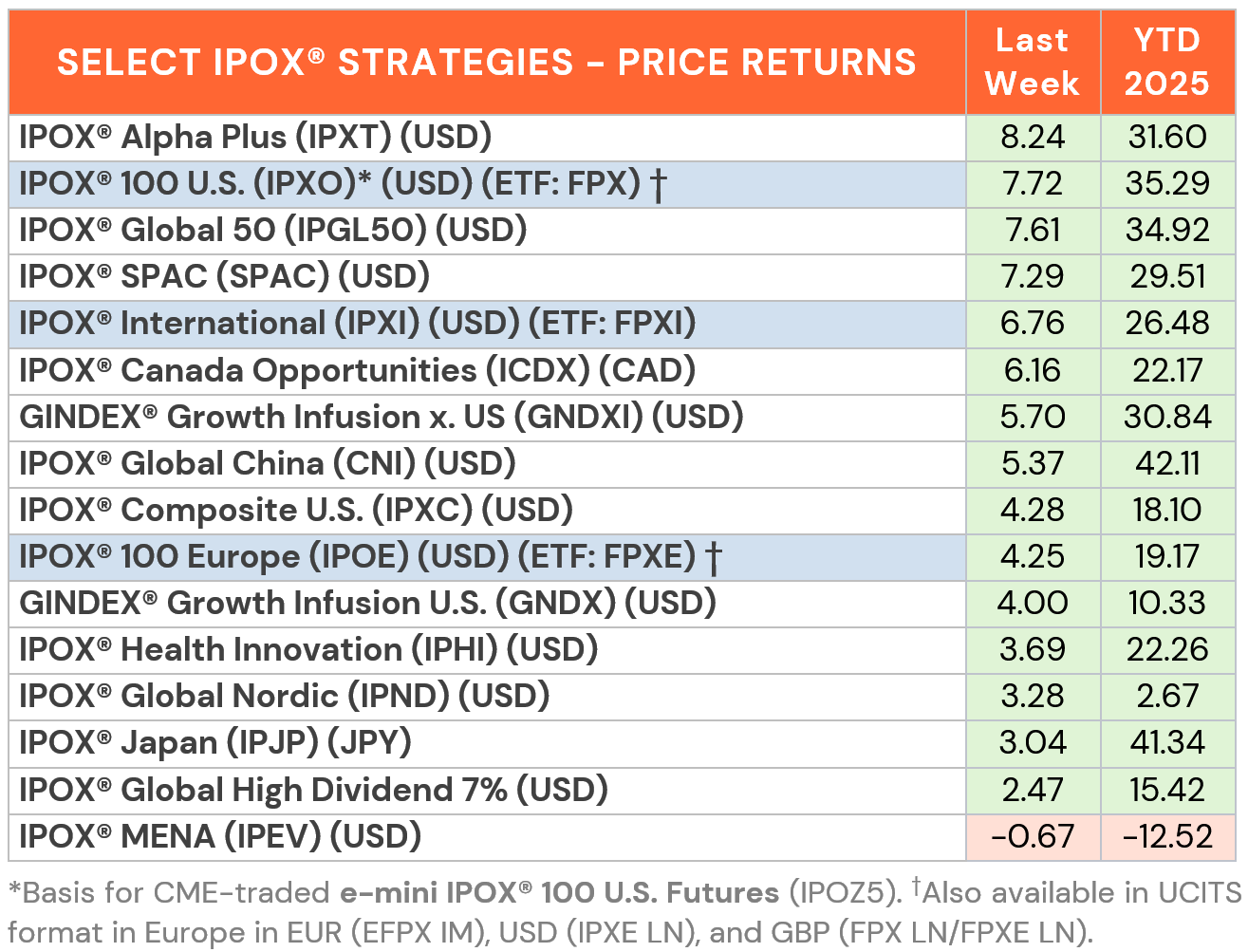

IPOX® 100 bounces back with a vengeance, soars +7.7% to +35.29% YTD.

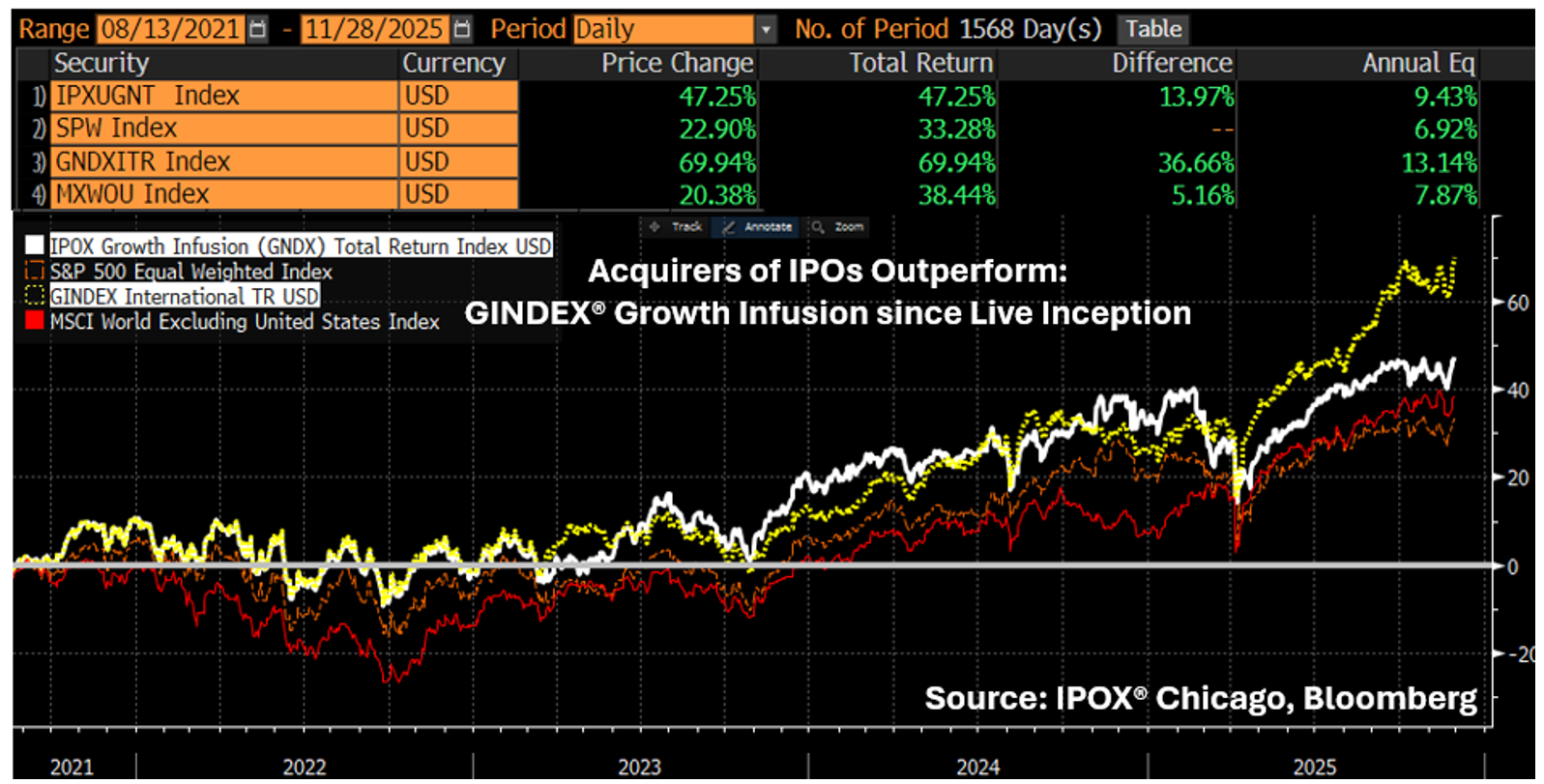

GINDEX® Growth Infusion Portfolios of IPO Acquirers set All-Time Highs.

Focus on: CRDO, LITE, HOOD, SNDK, VALT LN, HAG GY, THEON NA.

18 firms raise $1.76 billion. South Africa’s Cell C (CCD SJ) debuts strongly.

SUMMARY: The IPOX® Indexes bounced back with a vengeance during the shortened and light-volume U.S. trading week as equity risk (VIX US: -30.22%) plunged, crypto recovered, U.S. fixed income firmed amid further positive Momentum in Russia/Ukraine peace efforts. With the exception of weak MENA, bargain hunting after the recent sell-off and position squaring ahead of what is typically a firm seasonal period for U.S. large- and small-caps, propelled IPOX® to massive absolute and relative gains. Amid a wave of M&A for IPOX® Universe holdings, we note a fresh all-time high in U.S. (GNDX) and International (GNDXI) IPO acquires modelled in our innovative GINDEX® Growth Indexes.

FPX ETF’S BIG WEEK: The IPOX® 100 U.S. Index (ETF: FPX), efficient pre- and post-IPO U.S. performance replication benchmark and alternative way to make size, sector and style decisions in VC- and P/E-backed firms – rocketed +7.72% to +35.29% YTD last week, moving +1833 bps., +1428 bps. and +2267 bps. YTD ahead of benchmarks S&P 500 (SPX), Nasdaq 100 (NDX) and Russell 2000 (RTY), respectively. 96% of IPOX® 100 holdings rose, with the average (median) equally weighted stock adding +6.47% (+4.62%), lagging the applied market-cap weighted IPOX® 100 U.S. Index and underlying the impact of the bounce in heavyweights. Computer equipment makers Credo Technology (CRDO US: +33.04%) and Lumentum (LITE US: +27.22%), as well as online trading platform Robinhood (HOOD US: +19.75%) led the explosive gains, while key deSPACs (DAVE, SOFI, ASTS) rallied. Special note in regard to USB flash drive maker Sandisk (SNDK US: +11.49%) which became the 4th IPOX® 100 Holding to be added to the S&P 500 Index, Americas leading equity gauge.

GINDEX® GROWTH INFUSION PORTFOLIOS SET ALL-TIME HIGH: Amid the huge wave of M&A for IPOX® members, we note an All-Time High in portfolios tracking IPOX® Acquirers, both with a U.S. (GNDX) and International (GNDXI) domicile. “The acquisition of IPOs will be the key driver of growth for private and publicly-traded firms in the future. Our innovative GINDEX® portfolios position investors into the most successful firms pursuing IPO M&A”, noted IPOX® CEO J. Schuster.

BIG GAINS EXTENDS TO IPOX® EX-U.S.: Our non-U.S. focused portfolios mirrored the strong sentiment in IPOX® U.S. last week. Individual firms in focus included London-traded mining Spin-off Valterra Platinum (VALT LN: +17.67%) and Canada’s specialty online retailer Groupe Dynamite (GRGD CT: +16.57%), while defense plays Hensoldt (HAG GY: -5.72%) and Theon (THEON NA: -1.51%) weakened further.

SPACS ARE HERE TO STAY: The IPOX® SPAC (SPAC) reversed sharply last week, surging +7.29% to 29.51% YTD. Bitcoin miner Cipher Mining (CIFR US: +43.82%) was the best performer following analyst upgrades, the launch of a 2x leveraged CIFR ETF amid the broad slump in risk. Online betting and gaming company Super Group (SGHC US: -9.45%) was the worst performer, declining after the U.K. gambling tax rate hike note. Two SPACs announced merger targets during the shortened trading week, including Soulpower Acquisition (SOUL US), which agreed to merge with international banking and stablecoin issuer Soul World Bank. No SPACs completed mergers, while two new SPAC IPOs were launched in the U.S. In media coverage, IPOX® CEO Josef Schuster commented on this week’s SPAC merger announcements of Enhanced, emphasizing that SPACs are here to stay and noting the strong recovery of select deSPACs this year driving interest.

ECM DEALS: 18 firms went public globally last week, raising a total of $1.76 billion. New listings delivered an average gain of +48.71% from their offer price (Median: +31.94%), with no deals launched in the U.S. Activity in accessible markets was led by Chinese aluminum producer Chuangxin Industries (2788 HK: +36.49%, $707 million offer). Other notable debuts included South African mobile network Cell C (CCD SJ: +16.98%, $155m), the Pharrell Williams-backed Japanese clothing brand HUMAN MADE (456A JP: +24.92%, $116m), and Romanian meat processor Cris-Tim (CFH RO: +7.39%, $103m). Chinese capacitor film producer Haiwei Electronic (9609 HK: -22.97%, $65m) struggled.

This week’s IPO Calendar features a diverse pipeline of global IPOs: AI-powered surgical tech firm UltraGreen.ai (UGAI SP) aims to raise $400 million in Singapore. Hong Kong will see listings from silicon wafer manufacturer Tianyu Semiconductor (2658 HK, $224m), noodle chain Xiao Noodles (2408 HK, $79m) and massage chair maker Lemo (2539 HK, $29m). In Australia, U.S.-domiciled spinal cord stimulation firm Saluda Medical (SLD AU) targets a $147 million raise, joined by epilepsy monitoring tech firm Epiminder (EPI AU, $82m). Other notable listings include Saudi car rental firm Cherry (CHERRY AB, $67m) and Samsung cancer biotech spin-off Aimed Bio (0009K0 KS, $48m) in Seoul.